Performance statement

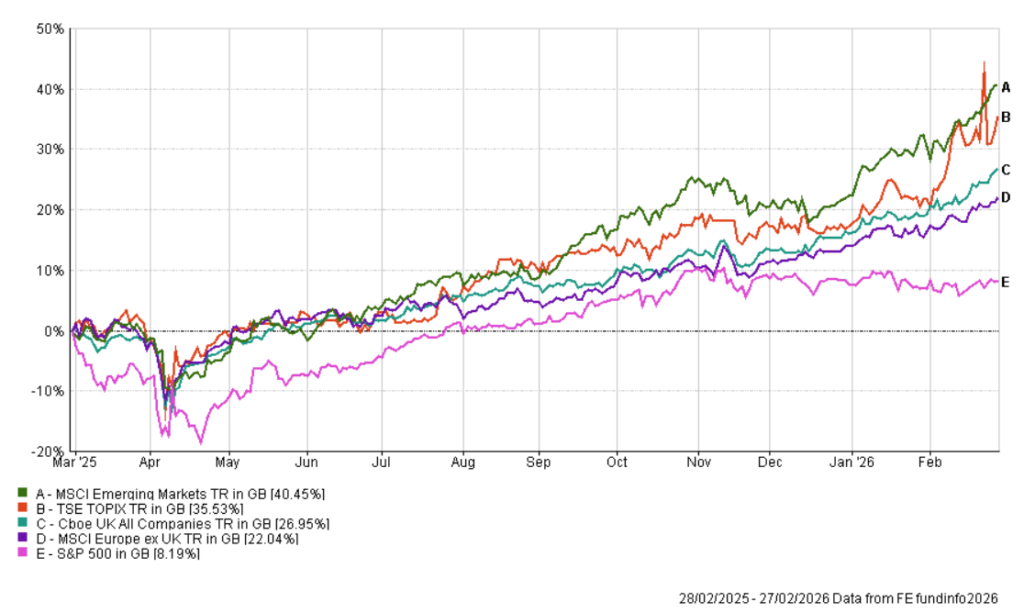

The IFSL Wise Multi-Asset Growth Fund returned 25.6% for the 12 months to the end of February 2026, marginally behind the CBOE UK All Companies Index (+27%) and ahead of its peer group, the IA Flexible Investment Sector (+15.3%).

Over the 5-year time horizon we consider sensible to look at our performance and as per our objective, the Fund is up 55.7%, behind the CBOE UK All Companies Index (+91.6%) but well ahead of the IA Flexible Investment Sector (+38.8%). The Fund sits in the top quartile of funds in the peer group over that time horizon, which is a pleasing outcome given the broad challenges thrown at investors during the period (aftermath of the Covid pandemic, wars, political changes, dominance of large technology companies, sharp shifts in interest rates, trade wars, etc…) and the many headwinds faced by investment trusts (our main focus).The IFSL Wise Multi-Asset Growth Fund returned 11.5% for the year to the end of February 2025, behind the CBOE UK All Companies Index (+18%) but ahead of its peer group, the IA Flexible Investment Sector (+9.7%).

Market Review

The period in review has been shaped by a combination of economic fundamentals, political shocks and policy unpredictability. Donald Trump’s second mandate has again redefined the balance between economics and geopolitics, with tariffs, trade negotiations, and unconventional policymaking driving sentiment across asset classes. While creating some shocks along the way, investors have increasingly become accustomed to Trump’s unconventional governing style, possibly leading to a degree of complacency regarding general market risk.

At the centre of this period stood the global tariff saga, widely telegraphed by Trump during his campaign and culminating in the so-called “Liberation Day” announcement on April 2nd. Tariffs are taxes on imports from another country, used as a means to favour domestic companies by making their foreign competitors more expensive. As such, they fit into Trump’s mandate of “making America great again”. Expectations were that those tariffs would be justified and targeted, however. Instead, the tariffs announced on April 2nd were broadly incoherent and global, muddying the message and creating uncertainty. Trump’s administration initially appeared to use trade deficits (when a country imports more goods and services than it exports) as a proxy for unfair trade practices. While there are many unfair practices the US can claim to have been the victim of, particularly from China, which would justify some retaliation, trade deficits themselves are not unreasonable if goods cannot be manufactured domestically or if consumers want products that are more cheaply manufactured abroad. Equating deficit and unfairness is thus a gross simplification at best. Over the weeks following the announcement, however, it became clear that, rather than being driven by ideological or economic rationales, tariffs are used by Trump as a profit maximisation exercise (via the increase in taxes collected by the US government), using the US clout to bully international partners into submission. The result was volatility spikes of an extraordinary magnitude, followed by equally rapid recoveries as concessions, pauses, or new negotiation deadlines were announced. Markets learned that while Trump’s threats could not be ignored, overreacting risked missing the equally sudden reversals. The international response to US policy, on the whole, was one of accommodation and submission, as opposed to confrontation. As such, trade deals were struck with the UK, the EU, Japan and South Korea amongst others ahead of deadlines set by Trump, thus preventing what could have been nasty trade wars. By the end of the period, however, the US Supreme Court ruled that presidents lack legal authority to impose sweeping tariffs, clarifying that this authority belongs to Congress and rendering the Liberation Day tariffs illegal. Following a Federal Reserve (the US central bank) report that about 90% of tariffs were borne by American businesses and consumers through higher end prices rather than by foreign companies, the ruling itself could be perceived as the equivalent of striking down a government for implementing an illegal consumption tax. The Supreme Court did not rule on the question of refunds, however, opening the door to further litigation. Meanwhile, immediately after the Supreme Court ruling, President Trump announced a new temporary blanket global tariff of 10%, valid for a maximum of 150 days during which the administration will no doubt look for a legal way to tax imports. This new regime threw the trade deals agreed earlier into question with some countries, including the UK and the EU, ending worse off despite having made hard concessions than counterparts such as Brazil and China, which resisted pressure from Trump.

Geopolitics were lively too during the period with developments that could reshape the global order established after WWII. The unexpected capture and removal of President Maduro in Venezuela by US military forces raised legal questions and made other countries uneasy. This was overshadowed by rising tensions between Trump and European countries over Greenland. These tensions led to tariff threats between the US and the EU, unusually strong public arguments between allied leaders, and concerns about the possible weakening of NATO, the military alliance of European and North American countries that has ensured the security of its members for nearly 80 years. After strong resistance from international partners, Trump seemed to back down towards the end of the period. However, such aggressive behaviour from a NATO member may encourage other Western countries to reduce their dependence on the US, both militarily and economically. It is therefore notable that both Prime Minister Carney of Canada and Prime Minister Starmer of the UK made official visits to China for the first time in about eight years to discuss possible trade agreements. At the end of the period, after weeks of the US showing military strength in the Middle East and issuing threats against Iran following deadly protests, a full-on war erupted which quickly spread across the region.

On the economic front, the “One Big Beautiful Bill Act,” promising tax cuts but threatening trillions in new debt, underscored investors’ unease with US fiscal discipline, a theme prevalent on both sides of the Atlantic. For the reporting period, the US economy continued to prove resilient in the face of uncertainty, with reports of strong GDP growth and solid employment numbers. There were some signs of waning at the end of the period though, particularly visible in weaker consumer confidence, hurt by sustainably high cost-of-living and heightened uncertainty. This led Trump to increasingly pressurise the central bank (the Federal Reserve or the Fed) to cut interest rates more aggressively than the three cuts it delivered over the year, resorting to personal attacks on some of its governors and its chairman in a perceived threat to the Fed’s independence, which spooked financial markets. Facing strong bipartisan and investors pushback, Trump nominated a credible and moderate candidate to take over as chair of the central bank in June, hopefully thus preserving the credibility of one of the pillars of global financial stability.

In the UK, we end the period with an unstable political balance with Prime Minister Starmer under pressure from his own MPs after a series of policy U-turns leaving the government weak and, largely, directionless. The dreaded autumn Budget offered yet another increase in spending and taxes while offering little in terms of growth-boosting measures, but it at least managed to beat the worst-case scenario markets had priced in going into the event. Like in the US, the Bank of England delivered three rate cuts over the year, willing to boost anaemic growth but wary of stubbornly high inflation. Towards the end of the period, however, inflation started falling more than expected leaving the door open for more rate cuts in the months ahead. In Europe, like in the UK and the US, fiscal debates also reached boiling point, most notably in France where the government lacks a majority and opposition parties are playing for time until the next presidential election in 2027. This was in contrast to Germany where a new Chancellor managed to break the country’s reluctance to use debt as a financing tool and pushed for up to 1 trillion Euro extra spending in defence and infrastructure over the next few years. Japan was not immune from fiscal questioning either but, for now, investor sentiment is supported by the prospect of a stable pro-growth government following the landslide victory of Sanae Takaichi in the February snap general election. It remains to be seen how long it will take for concerns about the viability of her fiscal stimulus and tax cutting plans to emerge.

Amid this swirl of risks, markets have shown a paradoxical resilience. Equities across major regions pushed to record highs, propelled by a combination of corporate earnings strength, relief over avoided crises, and expectations of eventual monetary easing. At the same time, gold too traded at historic peaks, a hedge against the very risks equity investors seemed willing to overlook. This unusual cohabitation of exuberance and caution suggests markets are torn between optimism about growth and innovation, and fear of political and fiscal instability. There could be signs that vulnerabilities are growing under the surface, which would point to an environment where complacency could prove costly. In the second half of the reporting period, some cracks started to appear in the otherwise bullet-proof US equity market until then pulled inexorably higher by large technology companies. Investors seem increasingly worried about the scale of expenditure plans from big tech companies on AI-related projects such as data centres. While most of this spending can be financed by corporate cashflows, the increasing use of debt is causing concerns about overspending in a technology that is yet to prove it can be monetized. As a result, all the so-called Magnificent Seven companies (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) ended the period below their peaks, some of which reached as far back as October. While there are concerns about overspending and whether AI will meet the lofty growth expectations already priced in, there are also worries about how AI will disrupt adjacent businesses. Announcements of breakthroughs from a few AI developers in sectors such as legal, tax and accounting services, and wealth management caused a sharp decline in software companies. The fear is that corporate clients of these software companies will soon be able to pay a fraction of their subscription cost to an AI agent for equivalent results, potentially rendering incumbent service providers redundant. For now, markets are neither willing nor able to discern between winners and losers in the AI revolution causing global software companies to fall by a third from peak-to-trough. While overall equity and bond markets volatility remains benign, it is interesting to observe that the narrative may be changing. The background of strong economic growth in the US, coupled with fiscal and monetary stimulus remains a favourable one for so called risk assets (equities, bonds, commodities), but the market leadership is broadening out from the very concentrated markets that have dominated for the past few years. Developed markets outside of the US and emerging markets have thus strongly outperformed the US this year, for the first time since 2022 when technology companies last struggled. Time will tell whether this is a blip or the start of a durable rotation.

Fund Performance Review

The Fund delivered a return of 25.6% over the year thanks to our diversified exposure outside of US equities, the outperformance of the value versus growth style, a re-found interest in investment trusts and strong manager selection.

Addressing these factors in order, it is worth pointing out that, for now at least, the US outperformance relative to the rest of the world in equities is having a pause. The uncertainty caused by the reappointment of Trump in the White House and his often-chaotic leadership style have led investors to question the durability of American exceptionalism (the strong outperformance of the US economy and equity market over the past few years). While reported earnings from US companies continue to outpace the rest of the developed world’s, we may increasingly be reaching the point where they struggle to exceed expectations and justify the high valuations attributed to them. As such, the Magnificent Seven companies mentioned earlier appear to have peaked for now and concerns about technology companies in general (representing about a third of the US equity market] ) are rising. Moreover, the biggest casualty of Trump’s tariffs so far has been the US dollar, down 9% against a trade-weighted basket of currencies over the period. This is starting to push investors to consider alternatives to US assets by fear that the capital value of their investments gets wiped out by currency depreciation. In this new paradigm, for the pound sterling investor, each of UK equities, European equities, Japanese equities and emerging markets equities has materially outperformed US equities in the year. These moves are still very much in their early days after years of underperformance and are likely to gather momentum when more widely acknowledged. As a result, our allocations to all of those regions benefitted our performance, both in absolute terms and relative to our peers who largely remain overweighted US equities.

Source: FE, 28th February 2026

Another interesting driver of our performance during the period was the outperformance of value investing, outside of the US. Performance in the latter, while starting to broaden particularly since Q4 2025, remains heavily driven by large technology companies, which tend to be growth rather than value oriented. Value investors (of which we are one) tend to compare companies’ share prices today relative to their fundamentals, while growth investors focus on finding companies that can grow faster than their peers, thus commanding higher near-term valuations than value stocks. Because growth stocks are dependent on how their earnings will grow in the future, uncertainty over their structural growth drivers and higher interest rates tend to hurt their share prices (at a higher interest rate, the threshold is higher for earnings growth to justify a given rating). Comparatively, value stocks tend to outperform in such an environment because they are more dependent on present conditions (i.e. the value of their existing assets) than on the future (i.e. how their earnings will grow in the next few years). While benchmark interest rates have been cut by the main central banks over the period, fears about inflation and fiscal deficits have put some pressure on longer-term bonds, keeping interest rates elevated and thus benefitting value strategies. Moreover, when concerns about valuations and talk of a bubble in growth sectors like technology start to spread, investors rotate into assets with more margin of safety, i.e. less highly valued names. As a result, over the period, value stocks in global equities ex-US have outperformed growth stocks by more than 20%.

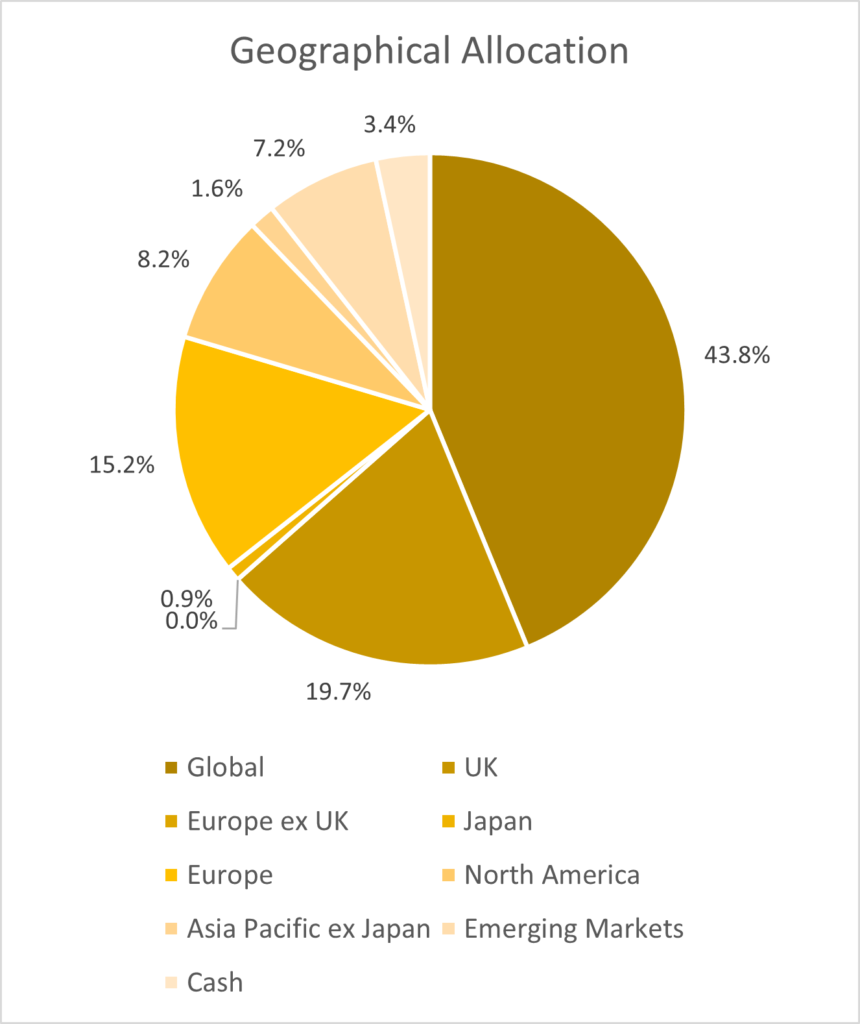

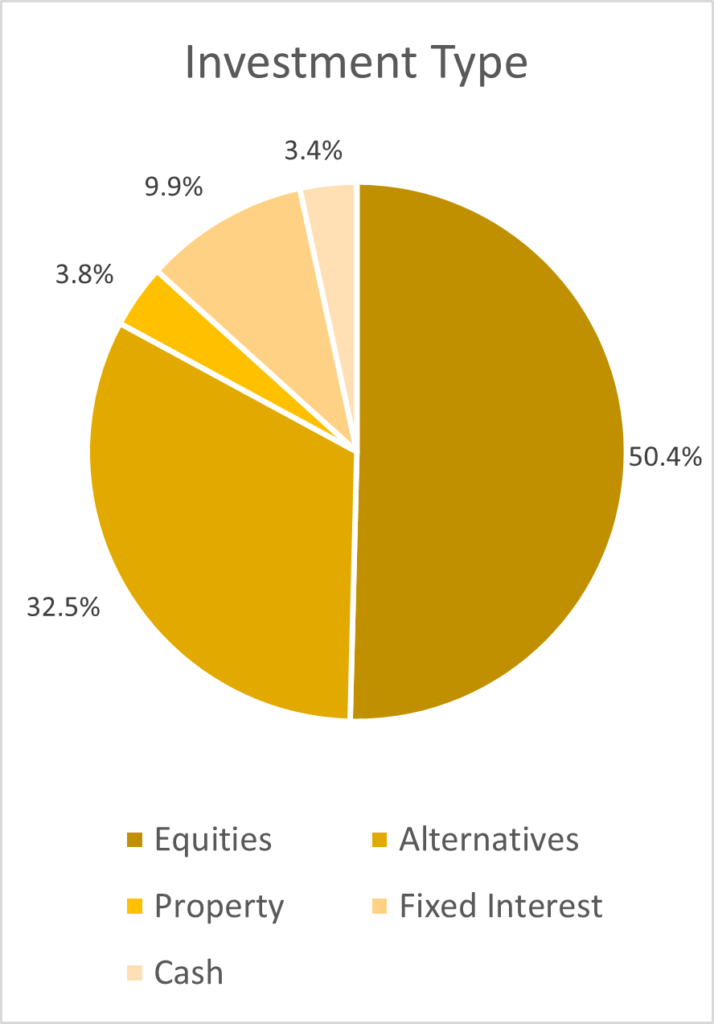

As our regular readers will know, the investment trust sector (close to 68% of our Fund at the end of the period) has suffered from headwinds for the past couple of years, including struggles in a rising rate environment for income strategies, a reduced investor base following consolidation in the wealth management sector, a dislike for UK assets where they are listed, and changes to cost disclosures. This had led to investment trusts discounts relative to their Net Asset Values (NAVs) to widen to historically high levels. This year, however, one can see early signs of a recovery, thanks to improved corporate governance leading to more investor-friendly changes (such share buybacks, tweaks to investment mandates, reduction in fees, redemption facilities…), corporate activism and mergers and acquisitions helping to sort out the wheat from the chaff. The FCA (Financial Conduct Authority) also finally confirmed the end of the double-counting of fees that plagued the sector for the past few years. As a result, discounts have continued to tighten since their historic trough a couple of years ago. For our Fund, over the reporting period, discounts reached an average trough of 18% in April and closed at 14%, still above our long-term average of 12% but moving in the right direction nonetheless.

Finally, in an environment where stock picking is getting increasingly difficult given the noise in financial markets, our ongoing focus on finding the best managers for each of our holdings proved fruitful during the period, helped both by their NAV performance and discount tightening, a sign that other investors are also acknowledging the quality of these funds. Notable performers were found across sectors, like in commodities with both Jupiter Gold & Silver (+186%) and BlackRock World Mining Trust (+125%). In regional equities, strong performers were found in the UK (Odyssean +29%, Fidelity Special Values +44%, Aberforth Smaller Companies +31%), in Europe (Lightman European +34%) and emerging markets (Templeton Emerging Markets +68%). We also had strong returns from our specialist managers like Ecofin Global Utilities & Infrastructure (+45%) and TR Property (+25%). Finally, after a few difficult years, it was pleasing to see our biotechnology names (International Biotechnology +39%, RTW Biotech Opportunities +45%) returning to form. While the start of Trump’s second mandate raised concerns for the sector (anti-vaccine stance, pressure on prices, doubts about the environment for research and development), most of those have now been lifted and as many new drugs were approved last year than in 2024. Crucially, last year was a record year for mergers and acquisitions (M&A) with biotechnology companies acquired at an average of 100% uplift and no sign of abating as large pharmaceutical companies need to replenish their expiring patents. Both of our biotech managers benefitted from that trend with a high single digit of their respective companies being acquired. Meanwhile, valuations remain attractive, albeit not as screamingly cheap as when we increased our conviction in the sector after the post-Covid hangover. Despite outperforming the main US equity by 15% last year (an appropriate comparator since most of the companies in the sector are US-based), the Biotechnology sector remains 30% behind the index over 5 years . We believe we are still at the foothills of the recovery.

There were no large detractors over the period. Achilles Investment Company (-1.5%), a small activist manager focusing on discount opportunities in the property and infrastructure sectors, had some early success but gave its gains back. Polar Capital Financials (-6%) was sold early in the year after a strong performance in 2024 but registered a small loss for the year at our exit point. Finally, our small basket of renewable energy trusts suffered from weak energy production, regulatory concerns and increased discount rates in the sector.

Portfolio activity

In a period that saw a number of shocks and increasing uncertainty, but also a general march higher in global equity and bond markets, we were active in recycling ideas in the portfolio and looking for new attractively valued positions. This led to five full exits (Polar Capital Global Financials Trust, Fidelity Asian Values, European Smaller Companies, Caledonia Investments and Schroder Emerging Markets Value). The first four of these were positions that we had been trimming on the way up for a number of months and had become relatively small. Each of these positions are from managers we have invested with for years and we continue to hold in high regard. They are thus likely to find their way back into the Fund in the future if valuations become more attractive. In the case of the Schroder fund, our decision to sell was caused by the surprise departure of its managers. In addition to those full exits, we also took profits in the strong contributors to performance we mentioned earlier with the biggest reductions being in Jupiter Gold & Silver Fund, BlackRock World Mining Trust (both trimmed by about 70% on the back of exceptional performance), Templeton Emerging Markets, Fidelity Special Values, AVI Japan Opportunity Trust, Ecofin Global Utilities and Infrastructure and Fidelity China Special Situations. We also reduced our position in the Schroder Global Recovery Fund as a diversifying measure following changes in the team.

Those proceeds helped increase our cash balance, particularly in the second half of the period when we got progressively wary of pockets of overexuberance in financial markets and some complacency from investors regarding valuation and political risks. We also reinvested into areas of greater upside potential. Some of those were in recently added positions we are still building up to full weight, such as Pershing Square Holdings, a high conviction value-oriented US equity manager, and RIT Capital Partners, a prudent and nimble manager of strategies in public and private assets, both trading at attractively wide discounts. We also added to our positions in TR Property Investment Trust which we think will continue to benefit from corporate activity (mergers and acquisitions, wind down of strategies…) and a re-rating of the property sector, particularly as AI is unlikely to disrupt this asset-heavy sector much. We also added to Mobius Investment Trust whose focus on small companies in emerging markets underperformed a tech-driven market. Lastly, we topped up Achilles Investment Company, an activist manager in the investment trust space, which we believe is well positioned to generate attractive returns despite uncertain macro conditions.

In addition to building up existing positions, a number of new managers were included in the Fund. Following the forced exit in the Schroder Emerging Markets Value Fund, we replaced it with another value-oriented manager on our reserve list: Pacific North of South Emerging Markets Equity Income Opportunities. We also diversified our holding in the Schroder Global Recovery Fund by switching some exposure into the Brickwood Global Value Fund (run by managers we have previously invested with in their previous firm). We added a new position in the CVC Income & Growth trust, a loan manager known for due diligence discipline and a strong default-avoidance track record. We built a basket of 6 infrastructure and renewables trusts, a sector that suffered from higher interest rates in the post-Covid area and went from trading at unsustainably high premiums to wide discounts. We think those are equally unsustainable now that portfolios have been revalued lower by managers, are more credible following increased disposals validating NAVs, and are offering attractive yields well in excess of cash. The sector is also starting to gather interest from activist shareholders and private buyers, which we think is likely to create a catalyst for a revaluation. Assets and strategies in those trusts are very idiosyncratic, which can make them difficult to differentiate, so we believe that a basket approach is sensible way to gain exposure. And finally, at the end of the period, we used some of the cash accumulated in previous months to take a new position in HG Capital Trust, the largest investor in private technology companies in Europe, which we used to own until the end of 2020 when valuations got too expensive for us. After a close to 30% fall in a matter of days during the fears of AI on software companies we mentioned in the market review, and with the discount widening to levels rarely seen in its 31-year history, we took the opportunity to start rebuilding a position. Whilst mainstream investors woke up to the AI threat only recently, the team at HG have been working with their underlying companies for years to develop and integrate their own AI capabilities and moats, which should put them on a strong footing for challenges ahead. It will surely take time for investors to get convinced this is indeed the case, so we have only taken a starter position for now but believe that this will be an attractive entry point for patient investors.

Investment Outlook

As the reporting period enfolded, it became increasingly clear that more and more investors are at least willing to question the US exceptionalism trade. The second presidential mandate of Donald Trump is leading to a rewriting of the international relations playbook which creates economic and geopolitical disruptions of a significant magnitude. While this does not necessarily jeopardize the US economy’s dominance on the global stage, it certainly has alerted investors to the risks of having portfolios with allocations concentrated in the US. The underperformance of US equities this year, early signs that large US tech companies may have peaked, and the concurrent strength in both risk assets like equities and defensive ones like gold, suggest some unease from the investment community and we are seeing the early signs of a broadening out of allocations away from the trades that have dominated for the past few years. The weakness in the US dollar is also a sign that global investors are looking for diversification. We believe that this presents a fantastic opportunity for our Fund which is underweight US equities and the giant technology companies, preferring diversifying undervalued assets. The performance of the recent months highlights that the assets we own are amongst the ones other investors are now scrambling to get access to, attracted by their quality and valuations. We are also encouraged by the fact that the vehicles we use to access those undervalued assets, investment trusts, are themselves undervalued, thus offering a double discount. With the investment trust sector now taking steps to address issues of oversupply of shares, irrelevance of some mandates and lack of shareholder consultation, we are optimistic that the seeds have been sown for a future improvement in the vitality of the sector. As ever, financial markets rarely move in straight lines and we are not ruling out the US which remains, after all, one of the greatest global growth engines despite political interference. We think, however, that the shocks created by the boundary-testing presidency of Trump are forcing investors to widen their opportunity set. A small reallocation out of expensive US equities into other assets would be sufficient to create a period of sustained strong performance. On the last day of our reporting period, after brewing for a few weeks, tensions between the US and Iran escalated to a full-on war, spreading across the region. It is too early to predict the direction of travel from here but this is likely to create volatility in financial markets and the impact on oil and gas markets in particular could have significant ramifications for global growth and inflation. Like we have for more than 20 years, we will continue to use the full flexibility of our mandate to ensure the most appropriate positioning in our Fund.

I would like to take this opportunity to thank our investors for their ongoing support. The whole Wise Funds team is at your disposal should you have any questions or would like to talk to us.

Vincent Ropers

Fund Manager

Wise Funds Limited

March 2026

TO LEARN MORE ABOUT THIS FUND , PLEASE CONTACT

01608 695 180 OR EMAIL JOHN.NEWTON@WISE-FUNDS.CO.UK

WWW.WISE-FUNDS.CO.UK

Full details of the IFSL Wise Funds, including risk warnings, are published in the IFSL Wise Funds Prospectus, the IFSL Wise Supplementary Information Document (SID) and the IFSL Wise Key Investor Information Documents (KIIDs) which are available on request and at wise-funds.co.uk/our funds The IFSL Wise Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. Capital appreciation in the early years will be adversely affected by the impact of initial charges and you should therefore regard y our investment as medium to long term. Every effort is taken to ensure the accuracy of the data used in this document but no warranties are given. Wise Funds Limited is authorised and regulated by the Financial Conduct Authority, No768269. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.

This presentation is for Professional Clients only and not for re-distribution.

All data is sourced by Wise Funds and any third party data is detailed on the specific page.