Performance Statement

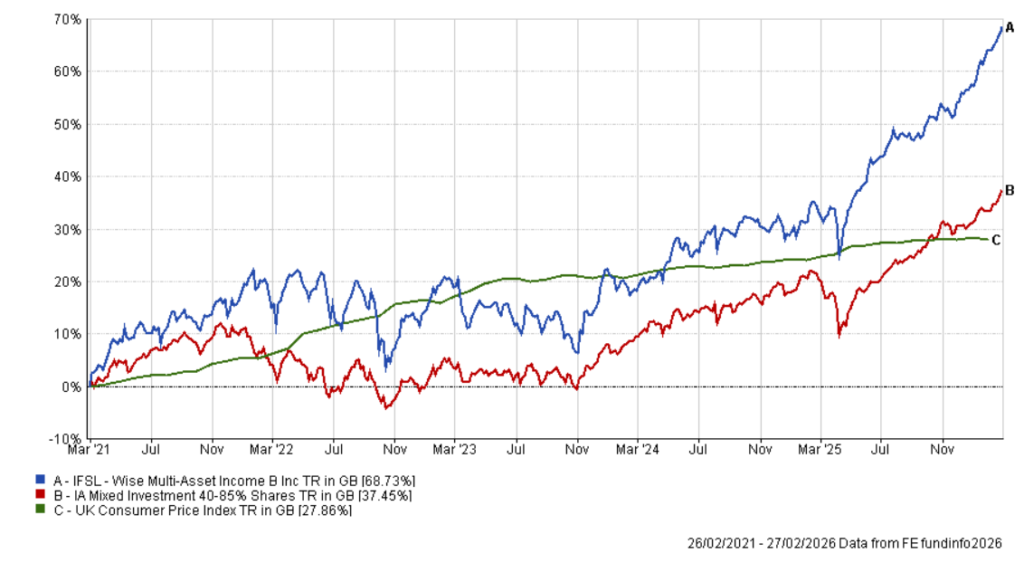

Over the 12-month period, the IFSL Wise Multi-Asset Income Fund rose 27.2% (B Income shares). Over this period, we outperformed the Consumer Price Index (CPI), which measures inflation and remains above the Bank of England target, up 2.6%. We also outperformed the comparator benchmark, the IA Mixed 40-85% Investment sector, which rose 14.5%. Over the 5-year time horizon we consider sensible to look at our performance and as per our objective, the Fund is up 68.7%, ahead of both CPI which rose 27.9% and our comparator benchmark, which rose 37.5%. The distribution per unit rose strongly by 10% from 6.1p to 6.7p over the year, more than making up for last year’s slight fall, which was impacted by one of our highest yielding holdings changing its dividend payment date around the fund’s year end. It remains the objective of the fund to increase the distribution per unit over 5-year rolling periods and we anticipate strong high single-digit growth over the forthcoming year. The prospective yield on the fund remains attractive at 4.9%.

Market Review

The period under review was characterised by a striking contrast between an increasingly uncertain political and geopolitical environment and the continued strength of global financial markets. Trade policy under the Trump administration introduced significant volatility, most notably around the “Liberation Day” tariffs, while a more transactional approach to foreign policy and rising geopolitical tensions raised questions about the stability of the post-war international order. At the same time, concerns around fiscal sustainability and institutional independence added to the sense of a more fragile policy backdrop. Yet despite these developments, the global economy proved resilient and financial markets performed strongly. Investors increasingly looked through political rhetoric and short-term shocks, supported by robust corporate earnings, falling inflation and expectations of lower interest rates.

Trade policy was one of the defining features of the period and offered the clearest example of the policy environment investors had to navigate. Tariffs themselves were not a surprise. They had been widely discussed before President Trump’s election and markets had anticipated a tougher US stance on trade, particularly in relation to China. What proved more unsettling was the scale, breadth and unpredictability of the measures ultimately pursued once the administration was in office. Initial expectations had been that new tariffs would be carefully targeted at specific unfair practices. Instead, the United States (US) opted for sweeping and unexpectedly draconian measures. The most important moment came with the April “Liberation Day” package, which imposed a 10% tax on nearly all imports outside of Canada and Mexico alongside surcharges on countries running trade surpluses with the US. This proved materially worse than many investors had expected and turned what had been anticipated as selective intervention into a much broader policy shock. At the outset the policy was framed around the idea that trade deficits represented evidence of unfairness by trading partners. Over time this justification looked increasingly questionable. Tariffs appeared to be used less as instruments of economic correction and more as tools for extracting concessions or raising revenue. By the end of the period this revenue-raising dimension had become increasingly evident, particularly as legal and fiscal questions surrounding the tariff regime came into focus.

Financial markets reacted in a pattern that became familiar. The initial announcement of the Liberation Day tariffs triggered a sharp sell-off in equities, a surge in volatility and record highs in gold prices. Investors were forced to confront the possibility that the administration might fully implement its most aggressive rhetoric. However, this was followed by a climbdown as exemptions and delays were introduced, allowing markets to recover once the worst-case scenario appeared less likely. Over time this sequence—aggressive announcements followed by market turbulence and eventual policy softening—became sufficiently consistent that traders coined the acronym “TACO”, shorthand for “Trump Always Chickens Out”. The phrase captured the perception that the administration’s opening stance often represented an extreme negotiating position rather than a settled policy outcome. Investors increasingly learned to look through the initial shock, waiting to see whether rhetoric would ultimately translate into policy. Nevertheless, the cumulative impact of uncertainty remained significant. Companies struggled to plan around shifting costs, supply chains were unsettled and the predictability of US economic policy was undermined. Financial markets themselves appeared to act as a constraint on policy. When tariff threats pushed bond yields higher and tightened financial conditions, the administration repeatedly softened or postponed measures, reinforcing the sense that markets were acting as a disciplining force.

The international response was notable for its pragmatism. Rather than escalating into a full-scale trade war, many countries pursued accommodation rather than retaliation. The European Union, Japan and Vietnam pledged to increase imports of US goods or channel investment into American industries, while corporations sought exemptions or carve-outs. Negotiations therefore became a defining feature of the period. Tariffs were repeatedly used as leverage to extract concessions, while trading partners attempted to limit the fallout through pledges, investment commitments or increased purchases of US goods. Many of these commitments lacked detail or enforceability, leaving underlying uncertainty unresolved.

By the end of the period the legal basis of the tariff regime itself had come under pressure. The US Supreme Court ruled that President Trump had exceeded his authority in imposing many tariffs without Congressional approval. This potentially called into question more than $150bn of future tariff revenue and opened the possibility of corporate lawsuits seeking refunds for tariffs already paid. The administration responded by introducing temporary blanket tariffs of 10% lasting up to 150 days without Congressional approval. However, the measure appeared poorly calibrated, potentially penalising countries that had previously negotiated constructively with Washington while leaving those with larger trade deficits relatively unaffected. Another increasingly prominent issue was who ultimately bears the cost of tariffs. The administration argued that foreign exporters would pay. However, a Federal Reserve study suggested that around 90% of tariff costs were ultimately borne by US companies or consumers. Economically this reinforced the view that tariffs function as a domestic tax, adding to inflationary pressure. Politically it risked eroding support for the policy as the mid-term elections approached.

Geopolitics also became an increasingly important theme, reflecting a broader shift in US foreign policy. A consistent thread throughout the administration’s approach was the belief that the United States had been disproportionately subsidising the prosperity and security of other nations. President Trump repeatedly argued that allies had benefited from US protection, open markets and innovation while contributing insufficiently themselves. This philosophy translated into a foreign policy focused on prioritising US interests and reassessing long-standing international commitments. The most visible example was the administration’s approach to NATO. Trump repeatedly criticised allies for failing to meet defence spending commitments, arguing that the United States had effectively been underwriting European security.

The result was a shift in European defence policy. NATO partners pledged increased military spending to maintain Washington’s support, while Germany approved unprecedented plans to spend up to €1 trillion on defence and infrastructure. The war in Ukraine further illustrated these shifting dynamics. The breakdown of a minerals agreement with Ukraine and the suspension of US military aid raised questions about the durability of Western security commitments. For much of the conflict Ukraine had relied heavily on American financial and military support. The interruption of that support therefore reinforced the perception that the United States was becoming more selective about its global commitments.

The administration’s economic diplomacy reflected a similar philosophy. Just as Trump argued that the United States had subsidised global security through NATO, he also claimed that American consumers had subsidised global economic growth. Pharmaceutical pricing became a prominent example. Washington argued that US patients were effectively paying for the research and development that allowed other countries to access medicines more cheaply. Negotiations with pharmaceutical companies therefore aimed to reduce prices for American consumers, sometimes in exchange for trade concessions. This transactional approach was also visible in direct geopolitical actions. Early in 2026 the unexpected removal of Venezuelan president Nicolás Maduro shocked observers. Although concerns about the regime’s legitimacy had long existed, the operation was justified as a law-enforcement action rather than a military intervention, bypassing Congressional approval and raising legal questions. Another episode that unsettled allies was the dispute over Greenland. Trump’s suggestion that the United States might attempt to acquire Greenland—even potentially through military means—provoked strong reactions among NATO partners and challenged established diplomatic norms. The Middle East provided another source of uncertainty. Earlier US strikes on Iranian nuclear facilities briefly pushed oil prices higher before stability returned. However, domestic conditions inside Iran deteriorated sharply, with mass protests, severe repression and a collapsing currency creating an unstable environment. These tensions ultimately culminated in a major escalation when the United States and Israel launched strikes against Iran, triggering a wider regional conflict and raising concerns about disruption to global oil and LNG shipping routes. Although the operation occurred after markets had closed for the period under review, the immediate reaction in March was a sharp rise in energy prices and renewed fears about inflation.

Taken together, these developments illustrated how geopolitical risk had moved closer to the centre of the investment landscape. For decades the global economy benefited from relatively stable alliances and predictable security arrangements. Over the period under review that backdrop appeared less secure.

Despite this turbulent political environment, the economic backdrop proved resilient. Labour markets remained relatively strong, household balance sheets were healthy, governments increased investment and financial institutions were broadly stable. Even after the disruptive tariff announcements, global growth forecasts remained broadly unchanged for 2026. In the United States, economic activity remained supported by resilient consumer spending, accommodative financial conditions and expansive fiscal policy. Revised economic data confirmed stronger growth earlier in the year than initially reported, while employment remained broadly solid despite signs of softening later in the period. The most striking feature of US policy was the scale of fiscal support outside recessionary conditions. This culminated in the “One Big Beautiful Bill” (a law signed by Trump including various tax and spending policies), reinforcing expectations that fiscal deficits would remain unusually large and raising concerns about long-term debt sustainability. Institutional tensions also became more visible. President Trump repeatedly criticised Federal Reserve chair Jerome Powell and called for lower interest rates. The dismissal of the head of the Bureau of Labor Statistics after employment data revisions further unsettled markets and raised concerns that political pressure might compromise central bank independence. Despite these tensions, inflation data surprised on the downside and the Federal Reserve cut interest rates three times during the period, reducing rates by 0.75%. Markets increasingly expected further easing into 2026.

The UK experienced a similar combination of easing inflation and weakening growth. Economic growth contracted slightly during the autumn while indicators, such as consumer spending and construction activity, suggested a softening economy. Lower inflation allowed the Bank of England to cut interest rates by 0.75% over the period, with markets expecting rates to fall to around 3% by the end of 2026. Politically, however, the UK environment remained volatile. The Autumn Budget dominated sentiment, with speculation around weaker productivity, higher welfare spending and potential tax increases unsettling both voters and investors. Although the Budget confirmed higher taxation to fund increased spending, much of the fiscal tightening was pushed into later years, leaving ongoing concerns about fiscal credibility.

Europe began the period expecting a modest recovery supported by rising real incomes and lower inflation, and by year-end growth had stabilised. The July 2025 EU-US trade agreement reduced uncertainty while domestic demand strengthened as earlier monetary easing fed through to the economy. Germany played a central role after approving unprecedented defence and infrastructure spending, marking a significant shift away from its traditional fiscal conservatism. France remained politically unstable, with repeated leadership changes weighing on confidence. The European Central Bank cut rates to 2%, though markets increasingly believed the easing cycle was nearing completion.

Japan stood apart from other major developed economies. The Bank of Japan continued tightening policy, raising rates from 0.5% to 0.75% and signalling further increases. A more expansionary fiscal stance under Prime Minister Takaichi, including proposed tax cuts, combined with rising inflation to push Japanese government bond yields sharply higher, with spillover effects across global bond markets.

Despite political turbulence, global financial markets performed strongly. Equity markets delivered solid returns while credit markets remained resilient and volatility outside the tariff episode remained relatively subdued. Global equities were supported by resilient earnings, falling inflation and expectations of lower interest rates. However, the distribution of returns across regions revealed important shifts. Despite stronger earnings growth, US equities underperformed in relative terms, reflecting their higher starting valuations after several years of exceptional performance. Market concentration also remained unusually high. A small group of large, US-based technology companies accounted for a historically high weighting in global equity indices, leaving global benchmarks heavily exposed to a narrow segment of the market.

Artificial Intelligence (AI) remained a dominant investment theme. Early enthusiasm drove strong performance among companies supplying AI infrastructure, such as semiconductor and cloud computing firms. As the year progressed, however, investor attention shifted towards the scale of capital expenditure required to support the AI build-out. Rising spending plans by major technology companies raised questions about whether eventual economic returns would justify the enormous investment. Advances in AI also prompted investors to reassess certain software business models that could potentially be disrupted by rapidly improving AI systems. This contributed to increased volatility within parts of the technology sector and encouraged broader market leadership.

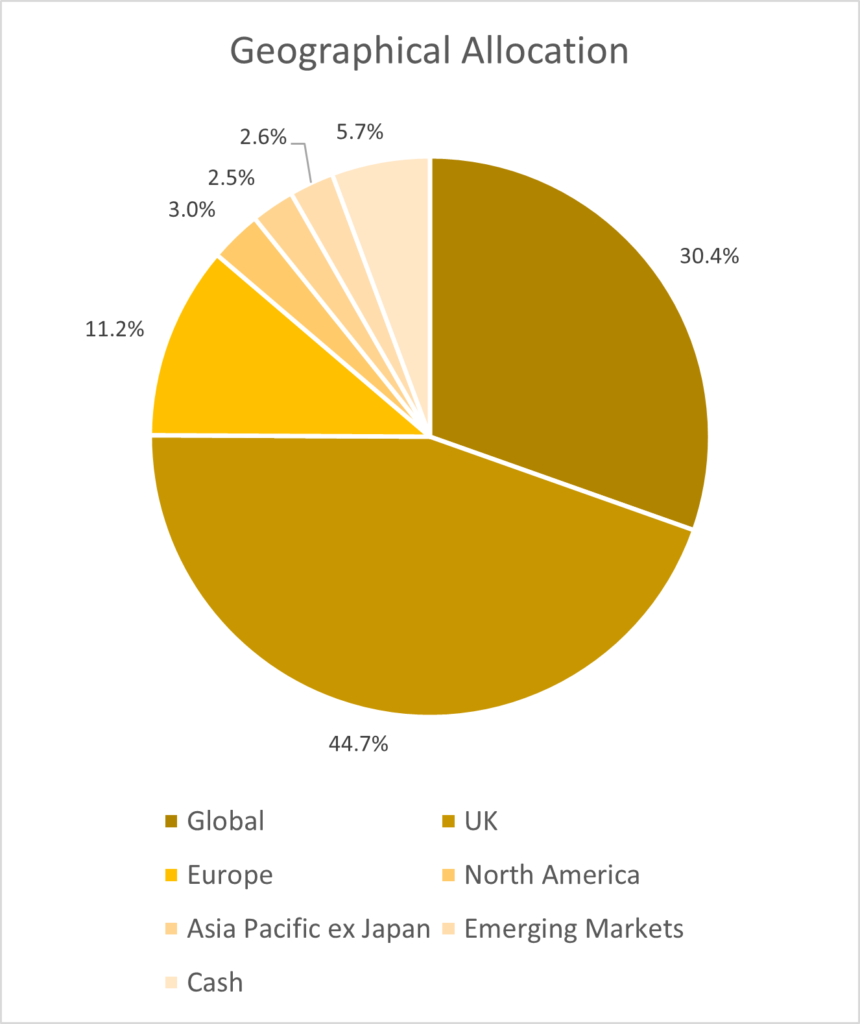

Investors increasingly looked beyond the US towards regions where valuations were more attractive and market concentration was lower. Japan, emerging markets and parts of Asia delivered strong returns, while UK equities also benefited from renewed interest. Currency movements reinforced these trends as weakness in the US dollar amplified returns from international markets.

Bond markets displayed a similar mix of optimism and caution. Corporate credit performed strongly as investor demand for yield remained robust. At the same time government bond markets reflected growing concerns about fiscal sustainability, with rising public debt pushing investors to demand greater compensation for holding longer-dated sovereign bonds.

Commodity markets showed greater divergence. Industrial metals linked to electrification and infrastructure investment performed well, while energy markets were more subdued. Gold stood out as a major beneficiary of geopolitical uncertainty, rising government debt and concerns about institutional stability.

Taken together, the period illustrated an unusual balance in the global investment environment. Political and geopolitical risks increased significantly, with trade conflicts, shifting alliances and institutional tensions creating a more uncertain policy backdrop. Yet economic fundamentals proved resilient. Labour markets remained relatively strong, inflation declined enough to allow interest-rate cuts in the US and UK, and fiscal policy continued to support growth. As a result, financial markets delivered strong returns despite an increasingly unstable political environment. Investors largely looked through political volatility and focused instead on the underlying economic backdrop. Nevertheless, the period also highlighted growing structural risks. Rising government debt, geopolitical tensions and pressure on institutions suggested that the long-term policy environment may become more complex. In such conditions, valuation discipline, diversification and active decision-making become increasingly important. While opportunities created by technological change and global growth remain significant, the investment landscape is likely to remain more uneven and unpredictable than in the past.

Performance Review

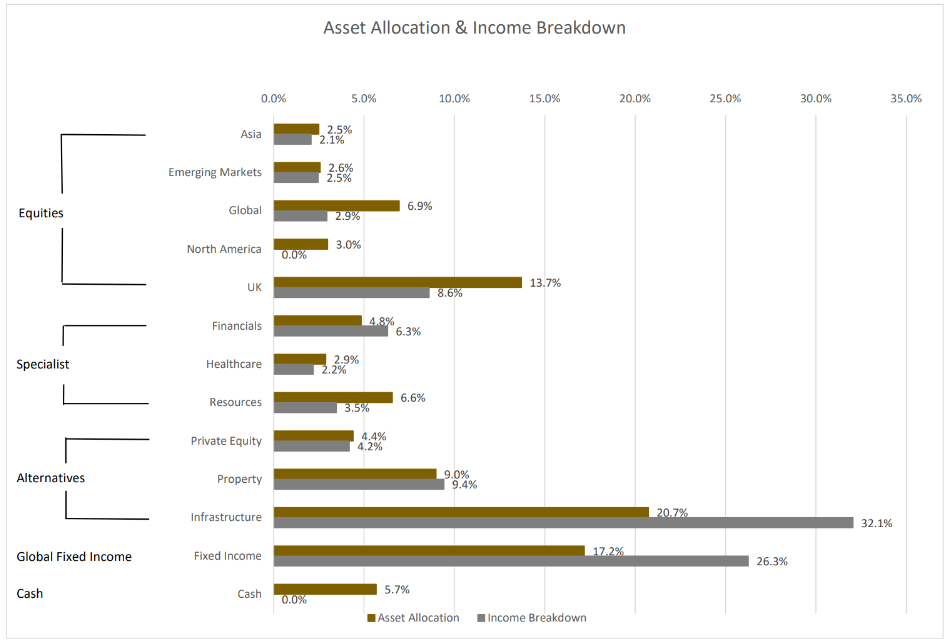

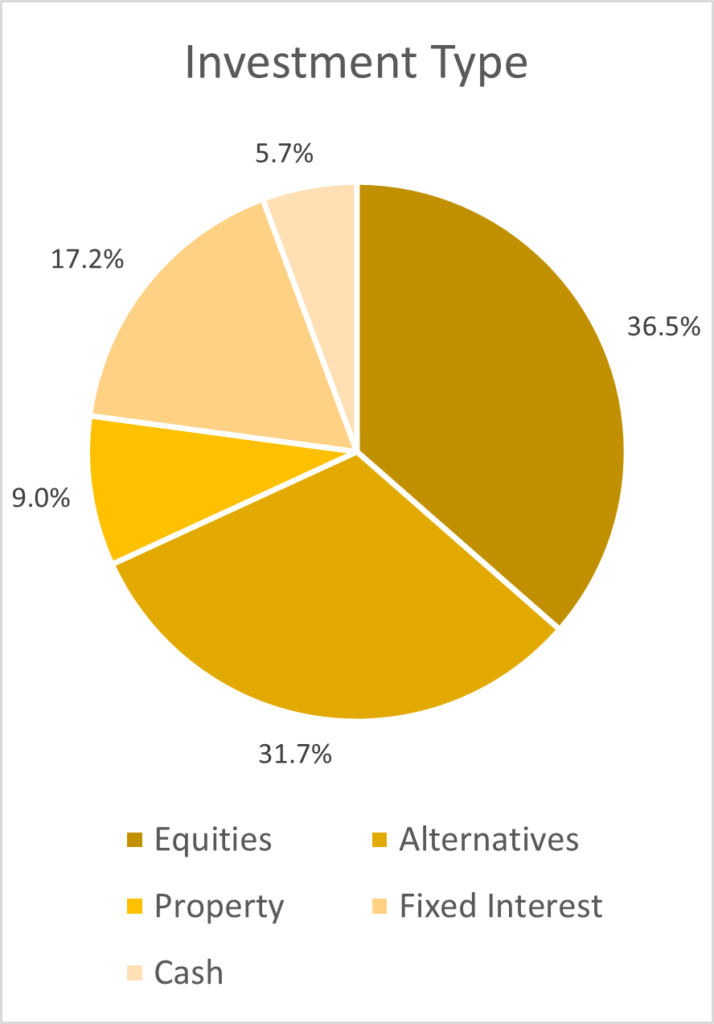

The fund delivered strong performance over the period, benefiting from the broadly favourable backdrop for risk assets. Equity markets advanced across most regions, commodity prices strengthened and credit markets remained resilient, providing a supportive environment for the portfolio’s exposure to commodities, infrastructure and international value equities. Performance was further supported by the rotation within global equity markets away from the highly concentrated US technology sector towards cheaper international markets. Several company-specific developments also contributed, including corporate activity in biotechnology and property and improving sentiment towards infrastructure assets trading on historically wide discounts. Detractors from performance were relatively limited and largely confined to the renewables sector.

The strongest performance came from our commodity-related investments, most notably BlackRock World Mining and BlackRock Energy & Resources. These funds benefited from rising commodity prices, particularly gold and copper, as well as discount narrowing as investor sentiment towards the sector improved. Gold remained in strong demand as investors sought protection against geopolitical risks, rising government deficits and concerns about central bank independence. Copper also performed well as supply constraints at major mines coincided with structurally strong demand from electrification, renewable infrastructure and broader industrial investment. Energy transition dynamics also supported the sector. The rapid expansion of AI infrastructure is expected to require significant additional electricity generation and transmission capacity, reinforcing the long-term investment case for resources linked to power generation, electrification and grid infrastructure.

Global equity markets were strong over the period and the fund benefited from its heavy overweight exposure to non-US markets driven by a focus on value fundamentals. Our UK equity holdings were particularly strong contributors. The fund’s four UK equity strategies—Aberforth Smaller Companies, Man GLG Income, Odyssean Investment Trust and Fidelity Special Values—all delivered strong returns and comfortably outperformed the broader UK market.

International equity holdings also contributed significantly. Middlefield Canadian Income was a notable contributor. In addition to the strength of the Canadian equity market and the trust’s exposure to resources and financial companies, performance was helped by the conversion of the vehicle from an investment trust where the daily price can deviate from net asset value (NAV) to a structure which more closely mirrors the underlying value. This allowed shareholders to benefit as the discount narrowed. Our emerging market strategies, Pacific North of South EM Equity Income and Schroder Emerging Markets Value, also performed strongly as investors favoured markets offering higher dividend yields, attractive valuations and stronger balance sheets. Aberdeen Asian Income and Prusik Asian Income also benefited from improving sentiment towards Asian markets and the continued emphasis on value-oriented strategies.

Within our specialist sector exposures, biotechnology was another important contributor to returns. International Biotechnology Trust delivered strong performance as the sector began to recover from an extended period of weak performance. Sentiment improved as large pharmaceutical companies accelerated acquisitions to replenish pipelines ahead of patent expiries. Several holdings within the trust were acquired at substantial premiums during the period while uniQure delivered highly positive clinical trial results in Huntington’s disease which drove its share price sharply higher.

The fund also benefited from exposure to financial companies. Holdings such as Polar Capital Global Financials, Legal & General and Paragon Banking Group delivered solid returns over the period. These businesses benefited from resilient earnings, strong capital positions and attractive dividend yields, which continued to appeal to income-focused investors.

Our holding in Ecofin Global Utilities & Infrastructure was another strong performer. The trust invests in listed utilities and infrastructure companies and benefited from growing recognition that the expansion of artificial intelligence infrastructure will require substantial investment in electricity generation and transmission networks, reinforcing the long-term growth outlook for regulated utilities.

Our core infrastructure holdings, HICL Infrastructure and International Public Partnerships, both contributed positively over the period, although performance diverged. The latter was the stronger of the two, benefiting from a resilient NAV, strong dividend cover and solid interim results supported by buybacks and disposals. Its commitment to projects such as the Sizewell C nuclear facility reinforced the long-term growth potential of the trust. HICL Infrastructure also benefited from stable operations and reliable income, but its relative performance was held back by the proposed merger with The Renewables Infrastructure Group (TRIG). Although presented as a way to create a larger and more diversified platform, the terms were widely viewed as favouring TRIG shareholders and the manager. HICL investors raised concerns around valuation, strategy and governance, and the deal was ultimately abandoned. The proposal was taken badly by the market and helps explain the relative underperformance of HICL versus International Public Partnerships over the period.

The fund’s property holdings delivered strong performance overall as sentiment towards the sector improved and corporate activity highlighted the underlying value within listed real estate. Consolidation remained a key theme, with several holdings receiving takeover approaches at significant premiums to prevailing share prices, including Urban Logistics, Care REIT, Empiric Student Property and Life Science REIT. Picton Property Income also initiated a strategic review with a view to putting itself up for sale.

Workspace Group initially detracted after reporting a reduction in NAV in its half-year results. However, the operational outlook appeared more encouraging, with improving enquiry conversion and tenant retention offering early signs that occupancy may be nearing a trough. Subsequent developments, including disposals of non-core properties and management changes, helped improve sentiment. Other holdings such as LondonMetric and Helical also performed well as sentiment towards the property sector improved against a backdrop of lower interest rates. Unite Group was a weaker performer as occupancy and rental growth disappointed for the academic year and pockets of oversupply emerged in certain student housing markets.

Our private equity holdings also contributed positively for much of the period, reflecting the improving outlook for portfolio realisations. ICG Enterprise Trustreported a steady increase in NAV supported by strong earnings growth and several major portfolio exits. Solid liquidity, ongoing share buybacks and consistent realisations achieved at or above carrying value helped narrow the discount and improve investor confidence. CT Private Equity also responded well to its latest results, with the underlying portfolio companies enjoying strong revenue and profit growth and the prospect of further NAV gains. Towards the end of the period sentiment towards the sector became more mixed, however, as investors became more cautious about private equity exposure to software companies amid concerns that advances in AI could challenge parts of the software sector. However, software represents a relatively small portion of the portfolios we hold (c.17% on average), both of which are broadly diversified across a variety of sectors.

The fund’s bond holdings also contributed positively to performance. TwentyFour Income Fund and GCP Infrastructure delivered solid returns as investor demand for income remained strong and credit markets remained resilient. The Premier Miton Strategic Monthly Income Bond Fund also delivered steady returns for a lower-risk strategy focused primarily on investment-grade bonds.

The principal area of weakness over the period was the renewables sector. Despite attractive dividend yields, total returns were impacted by falling NAV’s and widening discounts. Several factors contributed to the weak sentiment, including weaker wind generation, lower medium-term power price expectations, regulatory uncertainty and perceived political risks.

Company-specific developments compounded these pressures. Bluefield Solar Income initially announced that it had ended sale discussions and proposed a strategy involving the change of its management structure and a reduction in the dividend to fund future growth. The market reacted negatively and the board subsequently withdrew the proposal before launching a formal strategic review and sale process for the company. The sequence of announcements weighed heavily on the share price and further damaged sentiment towards the sector.

The abandoned merger between HICL Infrastructure and TRIG also contributed to weaker sentiment towards listed renewable and infrastructure assets more broadly. Although the long-term structural case for renewable energy remains intact, these developments left investor sentiment towards the sector extremely pessimistic over the period.

Portfolio Activity

Against a backdrop of elevated political and economic risks yet with global asset markets continuing to move higher, we were active in recycling the portfolio towards areas where we believed future returns relative to risk remained attractive.

Source: Wise Funds, 28th February 2026

A significant change to the portfolio during the period was the introduction and subsequent expansion of our renewable energy exposure. The sector had seen NAVs come under pressure for over two years as a result of higher bond yields, falling power prices and weaker generation than previously forecast. At the same time, listed renewable trusts had seen their share prices fall to historically wide discounts. This pattern has also been observed across other sectors that consist predominantly of physical assets, including property and core infrastructure, placing boards under pressure to demonstrate underlying asset values through disposals, corporate activity and strategic reviews. We believe the high dividend yields available within the sector—often around 10%—combined with wide discounts implied attractive medium-term returns for investors prepared to take a longer-term view.

Within property, our overall allocation remained broadly stable, but we actively recycled capital between holdings as corporate activity reshaped the sector. We exited several positions subject to takeover offers, including Urban Logistics, Care REIT and Empiric Student Property, which had received bids at substantial premiums to their prevailing share prices. We increased our exposure to Helical on weakness and initiated a position in Workspace, a London-focused provider of flexible office space. Workspace’s portfolio of smaller, flexible office units offers the potential to unlock value as occupancy improves and rental growth returns following a period of weak demand. Later in the period we also initiated a position in Picton Property Income, a diversified UK property company with a strong bias towards industrial assets. The company has been focused on increasing rental income as vacant space is let up and underlying rents rise.

Within equities, the overall allocation was reduced modestly following strong performance across many markets. Several holdings were trimmed where share prices had performed strongly and discounts had narrowed.

Periods of market volatility nevertheless created opportunities to redeploy capital and the sharp global market decline in April provided one such opportunity. We recycled capital from a lower-risk holding, TwentyFour Strategic Income, into International Biotechnology Trust and Odyssean Investment Trust.

Odyssean Investment Trust is a UK-focused equity strategy with a concentrated portfolio of mid-sized companies where the managers seek to unlock value through strategic, operational or managerial improvements. The portfolio is tilted towards technology and industrial businesses and has a significant proportion of overseas revenue exposure, reducing reliance on the domestic UK economy.

Our allocation to biotechnology was also increased early in the period through additional investment in International Biotechnology Trust. The sector had experienced an extended period of weak performance driven by tariff concerns and uncertainty around drug pricing. As sentiment began to recover and a wave of mergers and acquisitions by large pharmaceutical companies supported the sector, we subsequently took profits later in the year following the strong rebound in share prices.

Within Asian and emerging market equities, we made several changes to underlying managers. We sold our holding in Aberdeen Asian Income and replaced it with Prusik Asian Income, a differentiated value-focused strategy operating in a region where valuation dispersion between countries remains high. The strategy focuses on identifying attractively valued companies capable of delivering sustainable income growth.

We also sold Schroder Emerging Markets Value following the departure of the long-standing managers and reallocated the capital into Pacific North of South Emerging Markets Equity Income Opportunities, a strategy focused on attractively valued emerging market companies with strong cash generation and dividend yields.

In addition, we diversified our global value exposure by introducing Brickwood Global Value, funded through a reduction in our holding in Schroder Global Equity Income. The Brickwood strategy is managed by a team we have previously invested with at their former firm and focuses on identifying undervalued global companies where operational improvements or strategic change can unlock value.

Within Canadian equities, we reduced our exposure to Middlefield Canadian Income during its conversion from an investment trust trading at a discount into an exchange-traded fund structure trading closer to par. The narrowing of the discount provided an opportunity to realise gains following strong performance, although we retained a position given the positive outlook for the Canadian market.

Elsewhere within equities we reduced our holding in Paragon Banking Group following strong performance and also took profits in Fidelity Special Values afterboth strong underlying returns and a narrowing of the discount to NAV.

Within private equity, we reduced exposure following a strong period of performance. Both ICG Enterprise Trust and CT Private Equity were trimmed as discounts narrowed materially and valuations became less compelling following strong underlying portfolio performance.

Within commodities, we also took profits following a very strong run in resource equities. The weighting of BlackRock World Mining was reduced significantly despite the shares more than doubling over the period.

Within fixed income, we reduced our holdings in TwentyFour Income Fund and TwentyFour Strategic Income and increased our allocation to Premier Miton Strategic Monthly Income Bond Fund, which provides diversified exposure to investment grade and higher-yielding credit markets. We also initiated a position in CVC Income & Growth, a strategy investing in senior secured loans and other corporate credit opportunities.

Within infrastructure, we undertook a similar rotation out of strong performers into areas that had lagged but where we believed the valuation opportunity remained compelling. Following strong performance we reduced Ecofin Global Utilities & Infrastructure while initiating positions in The Renewables Infrastructure Group, Bluefield Solar and Foresight Environmental Infrastructure. We also reduced Pantheon Infrastructure and International Public Partnerships after strong performance but increased our holding in HICL Infrastructure, which had underperformed relatively.

As a result of these portfolio changes, we allowed the fund’s cash position to increase to 5.6%, providing flexibility to deploy capital should markets experience further bouts of volatility.

Outlook

Prior to the escalation of tensions with Iran, the outlook for the global economy had been gradually improving despite the disruption caused by trade tensions earlier in the year. While the new US administration introduced a more unstable policy backdrop through tariffs and institutional pressure, many of the fundamental drivers of economic growth remained supportive. Labour markets have proven more resilient than in past cycles, household and corporate balance sheets remain relatively healthy, and governments across many regions are stepping up investment, particularly in infrastructure and defence. At the same time, inflation has generally trended lower, allowing central banks in the US and UK to begin easing monetary policy. Taken together, these factors suggest that global growth should remain positive, even if somewhat slower than previously expected.

The recent conflict involving Iran introduces a new source of uncertainty, primarily through its potential impact on global energy markets. The temporary disruption to shipping through the Strait of Hormuz has pushed oil and liquefied natural gas prices higher, raising concerns that sustained energy price increases could slow growth and delay the decline in inflation. In a benign scenario, the Strait reopens relatively quickly and energy prices gradually return towards pre-conflict levels, resulting in only a modest impact on growth and inflation. A more prolonged disruption would present a greater challenge, potentially leading to a period of weaker growth and higher inflation, particularly in energy-importing economies such as Europe, the UK and Asia. However, there are reasons to believe that the conflict may ultimately remain contained. Higher oil and gas prices would risk fuelling inflation in the US ahead of the forthcoming mid-term elections, something the Trump administration will be keen to avoid.

Within this environment, we believe the fund remains well positioned to achieve its objective of delivering an attractive initial yield while growing both income and capital in real terms over time. In fixed income markets, real yields remain positive, providing a solid foundation for future returns, although tight credit spreads mean we continue to favour managers who are cautiously positioned. Within real assets, core infrastructure, renewables and property continue to offer the prospect of attractive income streams with the potential for dividend growth over time. In equity markets we remain active in managing exposures. We have reduced our overall allocation modestly and continue to maintain a highly differentiated exposure to markets where valuations remain attractive. After many years of exceptional performance by US equities, investors have begun to look more closely at opportunities in cheaper international markets, a trend that would benefit the fund given its current positioning.

I would like to take this opportunity to thank our investors for their ongoing support. The whole Wise Funds team is at your disposal should you have any questions or would like to talk to us.

Philip Matthews

Fund Manager

Wise Funds Limited

March 2026

TO LEARN MORE ABOUT THIS FUND , PLEASE CONTACT

01608 695 180 OR EMAIL JOHN.NEWTON@WISE-FUNDS.CO.UK

WWW.WISE-FUNDS.CO.UK

Full details of the IFSL Wise Funds, including risk warnings, are published in the IFSL Wise Funds Prospectus, the IFSL Wise Supplementary Information Document (SID) and the IFSL Wise Key Investor Information Documents (KIIDs) which are available on request and at wise-funds.co.uk/our funds The IFSL Wise Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. Capital appreciation in the early years will be adversely affected by the impact of initial charges and you should therefore regard your investment as medium to long term. Every effort is taken to ensure the accuracy of the data used in this document but no warranties are given. Wise Funds Limited is authorised and regulated by the Financial Conduct Authority, No768269. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.

This presentation is for Professional Clients only and not for re-distribution.

All data is sourced by Wise Funds and any third party data is detailed on the specific page.