For Professional Clients Only

Macro & Market Update

The past month has been dominated by a sharp escalation in the Middle East, where markets were caught off guard by the decision of the US and Israel to launch direct military action against Iran. Despite military manoeuvrings in the preceding weeks, this was unexpected given Trump’s prior positioning as a president intent on avoiding further overseas wars. The justification for intervention also appeared inconsistent with earlier claims that Iran’s nuclear capabilities had already been significantly degraded. From the outset, there has been little clarity over what would constitute a successful outcome, whether regime change or further degradation of Iran’s nuclear capability. Markets initially assumed a short-lived conflict, particularly given the political sensitivity of an inflation-driven cost-of-living shock ahead of upcoming US mid-term elections. However, that assumption has been challenged. Despite targeted strikes on senior leadership, the Iranian regime has proved more resilient than expected and has broadened the conflict regionally, including attacks on neighbouring countries and critical energy infrastructure. At the centre of both the geopolitical and economic picture is the Strait of Hormuz, which has become Iran’s primary source of leverage. Roughly a fifth of global oil and liquefied natural gas (LNG) flows through the Strait, making it the most important energy chokepoint in the world. Its effective closure has had immediate consequences: shipping has been disrupted, LNG exports curtailed, and supply chains affected beyond energy, including fertilisers and industrial gases. The market reaction intensified following Iranian strikes on Qatari LNG infrastructure, which undermined expectations of a short-lived disruption and led to a repricing in energy markets, implying a more prolonged impact. At the same time, Trump’s communication has been inconsistent — alternating between signalling ceasefires and threatening escalation, including potential strikes on Iranian energy assets or even the deployment of ground forces. While investors have been conditioned to discount some of his rhetoric following the Liberation Day tariff announcements last year, the risks of escalation in a military context are harder to control, contributing to repeated bouts of volatility. Politically, the conflict has exposed fractures within NATO, already strained by Trump’s aspirations over Greenland. Several allies have been reluctant to support US action, citing legal concerns and restricting access to bases and airspace. This raises broader questions about the durability of US support for Ukraine and increases the likelihood of higher defence spending across Europe. By contrast, China appears relatively well positioned, potentially benefiting from a more fragmented Western alliance.

The economic consequences have been most immediately visible in inflation expectations. The impact is uneven, however, with energy-importing economies — particularly in Europe, the UK and parts of emerging markets — being most exposed, while the US is relatively insulated due to greater energy independence. The shock is expected to weigh on global growth, with downside risks concentrated outside the US. This divergence has fed through into interest rate expectations. While central banks held interest rates unchanged, market expectations for the future direction for the remainder of the year have repriced sharply. In the US, expectations have shifted from around three rate cuts to no change — a move from easing to neutral. By contrast, the UK has seen the most dramatic adjustment, with expectations swinging from two cuts to two hikes, reflecting its exposure to imported energy inflation. Europe sits between the two, moving from stable rates to modest tightening. Investor hopes at the start of the year of further economic growth supported by further easing of monetary policy has unravelled as the month has progressed. Bond markets have responded accordingly. Yields have risen across the board, particularly in the UK, reflecting higher inflation expectations. Credit spreads (the premium corporates have to pay relative to governments) have widened, especially for lower-quality borrowers, though they remain below levels seen in previous periods of market stress. Importantly, higher starting yields provide a greater income buffer than during the Ukraine crisis. Risk assets have weakened in response to lower growth expectations, rising inflation and higher interest rates. Equity performance has diverged along energy lines, with the US more resilient and other regions, such as the UK, Europe and Emerging Markets underperforming, particularly domestically focused small and mid-cap stocks. Property has been notably weak reflecting higher bond yields and concerns over the impact of slower growth on rental demand. Commodity performance has been mixed. Oil has been the clear beneficiary from supply disruption, while copper has declined due to its economic sensitivity. Gold has failed to act as a safe haven, while the US dollar has strengthened. One relative area of resilience has been infrastructure, where inflation linkage and higher forward power prices have provided support, particularly within renewables. While not immune to rising bond yields, the sector has held up better than broader risk assets.

Fund Performance

Wise Multi-Asset Growth

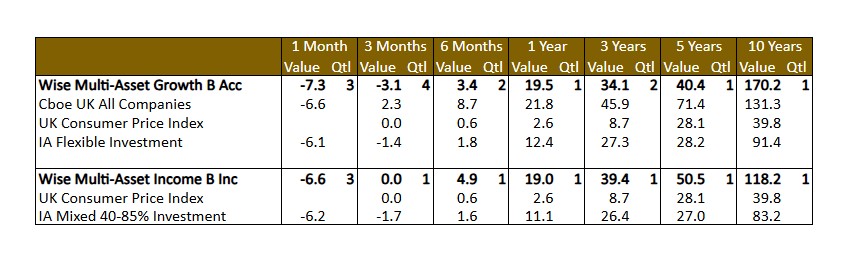

In March, the IFSL Wise Multi-Asset Growth Fund was down 7.3%, behind the CBOE UK All Companies Index (-6.6%) and its peer group, the IA Flexible Investment sector (-6.1%). In a difficult month, there were few places to hide. Our renewables and infrastructure basket protected capital, thanks to their defensive characteristics and being beneficiaries of rising power prices. Our bond managers, particularly Premier Miton Strategic Monthly Income Bond Fund and TwentyFour Strategic Income Fund benefitted from their active management of interest rate risk, as did Pacific G10 Macro Rates by actively taking advantage of short-term volatility. Finally, Pantheon International, after a weak start of the year, saw some recovery in its discount which helped its monthly performance.

Unfortunately, the list of detractors was long, particularly amongst investment trusts which suffered from discount widening on top of weakening net asset values (NAVs). UK equity names struggled in the challenging environment we described earlier for the country, as did TR Property given the sharp move higher in interest rates. Managers exposed to potentially hard-hit energy importers (Emerging Markets and Japan) and growth worries (Resources) also suffered. Gold did not play its safe haven role in this early stage, mainly due to the competition of rising yields, the stronger Dollar and to being a source of cash after an exceptional period of performance. The latter also applied to the biotechnology sector, despite a number of acquisitions at premium to carrying values announced in our funds over the month. Finally, private equity (other than Pantheon) continued to suffer partly from the AI concerns we mentioned in February.

Wise Multi-Asset Income

In March, the IFSL Wise Multi-Asset Income Fund fell 6.6%, marginally behind the IA Mixed Investment 40–85% sector, which fell 6.2%. This reverses year-to-date gains, leaving the fund flat versus a 1.7% decline for the benchmark. Equity, property, private equity and commodity holdings were the hardest hit, with Asian, Emerging Market, UK and financials exposures falling the most. Performance from our investment trusts was further impacted by widening discounts to net asset value, which we would expect to reverse over time. We saw stronger relative performance from Middlefield Canadian Enhanced Income, which benefits from oil & gas exposure, and BlackRock Energy & Resources. Our renewables positions also held up relatively well, supported by higher power prices, strong generation and inflation-linked subsidies offsetting higher bond yields. News flow from holdings was positive. HICL Infrastructure announced the disposal of a major French toll-road asset at a 21% premium to carrying value, highlighting the opportunity from its 27% discount. Elsewhere, three holdings within International Biotechnology Trust were subject to takeover bids at an average 70% premium, reflecting the continued need for large pharmaceutical companies to replenish their pipelines. In addition, Helical and Picton Property Income both reported positive lettings updates.

All data is in a total return format

Past performance is not a guide to future performance

Portfolio Changes

Wise Multi-Asset Growth

In terms of portfolio activity, given the unpredictability of the war, we tried to ensure the portfolio remained balanced between some defensive positioning and riskier positions. With President Trump’s style of managing geopolitics, there is as much danger from being over-exposed as being overly cautious. Our changes thus consisted in taking marginal profits (absolute and relative) where possible and redeploying gradually into areas we think were over penalised, such as Pershing Square, Blackrock World Mining, AVI Global, Aberforth Smaller Companies and TR Property. We also initiated a new position in Finsbury Growth & Income. Quality growth managers have had a torrid time for the past couple of years after a decade and a half of great performance. We think that valuations are looking more reasonable now (on the underlying assets and the trust itself), which could make companies with durable competitive advantage attractive again.

Wise Multi-Asset Income

Over the month, we selectively added to risk assets where valuations appear compelling. As examples, we increased exposure to Prusik Asian Income, where the portfolio valuation is now lower than in the depths of Covid, as well as Aberforth Smaller Companies and BlackRock World Mining, and initiated a position in Finsbury Growth & Income Trust. We also increased property exposure through British Land and TR Property, funded by disposals of Unite and Life Science Reit and reduction in more economically sensitive Workspace. Elsewhere, we added to defensive infrastructure positions where share prices have not reflected improvements in net asset values, including GCP Infrastructure, HICL Infrastructure and The Renewables Infrastructure Group.

TO LEARN MORE ABOUT THESE FUNDS, PLEASE CONTACT

01608 695 180 OR EMAIL JOHN.NEWTON@WISE-FUNDS.CO.UK

WWW.WISE-FUNDS.CO.UK

Full details of the IFSL Wise Funds, including risk warnings, are published in the IFSL Wise Funds Prospectus, the IFSL Wise Supplementary Information Document (SID) and the IFSL Wise Key Investor Information Documents (KIIDs) which are available on request and at wise-funds.co.uk/our funds. The IFSL Wise Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. Capital appreciation in the early years will be adversely affected by the impact of initial charges and you should therefore regard your investment as medium to long term. Every effort is taken to ensure the accuracy of the data used in this document but no warranties are given. Wise Funds Limited is authorised and regulated by the Financial Conduct Authority, No768269. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.