Wise Multi-Asset Income

Fund Ratings

Investment Objective

The Fund aims (after deduction of charges) to provide:

- an annual income in excess of 3%: and

- Income and capital growth (after income distributions) at least in line with the Consumer Price Index ("CPI"), over Rolling Periods of 5 years.

Fund Attributes

- A flexible, diversified portfolio that can invest in all asset classes.

- Targets an attractive and growing level of income.

- The portfolio invests both direct and through open and closed-ended funds.

- Adopts a value biased investment approach.

- Pays monthly

Investor Profile

- Seek an attractive level of income and the prospect of long term capital growth.

- Accept the risks associated with the volatile nature of an adventurous multi-asset investment.

- Plan to hold their investment for the long term, 5 years or more.

Key Details

| Target Benchmark | UK CPI |

|---|---|

| Comparator Benchmark (Sector) | IA 40-85% Investment Sector |

| Launch date | 3rd October 2005 |

| Fund value | 86.6 million |

| Holdings | 37 |

| Historic yield | 4.50% |

| Div ex dates | First day of every month |

| Div pay dates | Last day of following month |

| Valuation time | 12pm |

- Past performance is not a guide to the future and outperforming target benchmarks is not guaranteed.

- The historic yield reflects distributions over the past 12 months as a percentage of the price of the B share class as at 31ST May 2026. Investors my be subject to tax on their distributions.

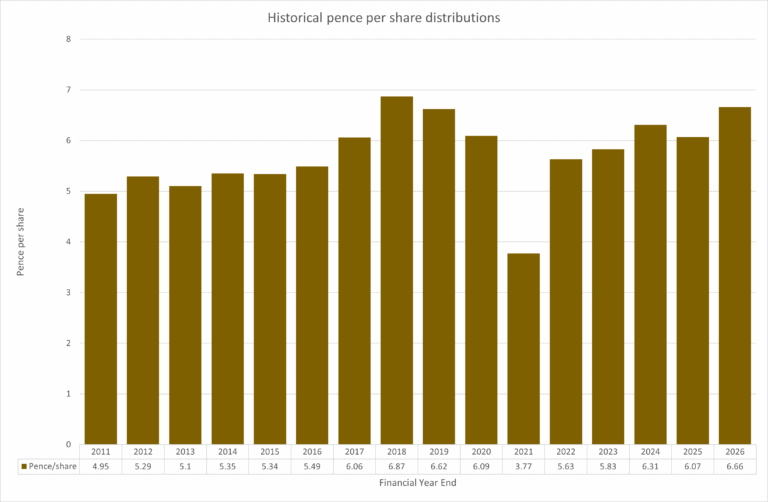

Dividend Information

Pence/share figures relate to the fund’s financial year ending in February of the relevant year.

For a breakdown of the dividends, please click here

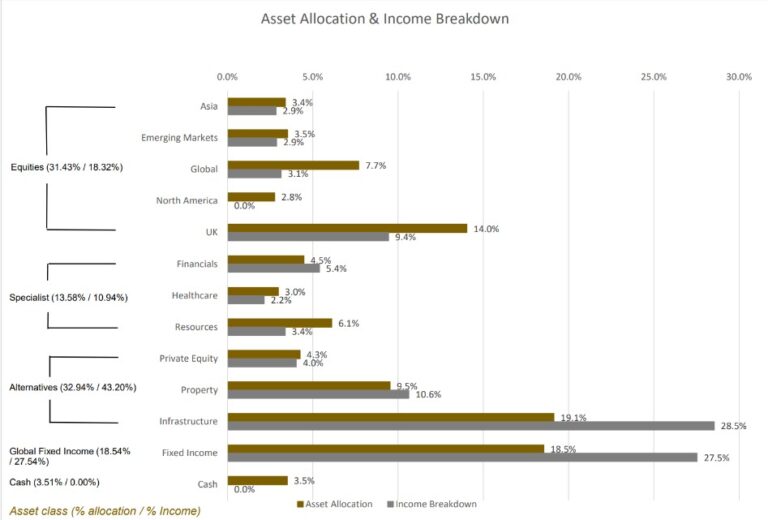

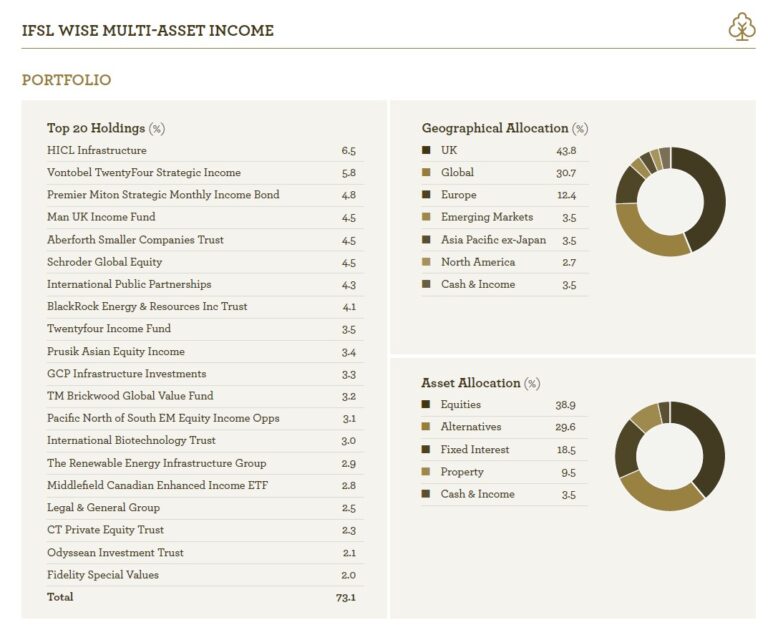

Investment Portfolio - May 2026

Source – Wise Funds Limited as at 31st May 2026.

The asset allocation is derived from the full portfolio holdings and the income data shows where the the current yield is being accrued from by asset class.

- Past performance is not a guide to the future

- Data as at 31st May 2026

Share Class Information

| | B Acc (Clean) | B Inc (Clean) | W Acc (Institutional) | W Inc (Institutional) |

|---|---|---|---|---|

| Sedol Codes | B0LJ1M4 | B0LJ016 | BD386V4 | BD386W5 |

| ISIN Codes | GB00B0LJ1M47 | GB00B0LJ0160 | GB00BD386V42 | GB00BD386W58 |

| Minimum Lump Sum | £1,000 | £1,000 | £50 million | £50 million |

| Initial Charge | 0% | 0% | 0% | 0% |

| IFA Legacy Trail Commission | Nil | Nil | Nil | Nil |

| Investment Management Fee | 0.75% | 0.75% | 0.50% | 0.50% |

| Operational Costs | 0.17% | 0.17% | 0.17% | 0.17% |

| Look-through Costs | 0.23% | 0.23% | 0.23% | 0.23% |

| Ongoing Charges Figure 12 | 1.15% | 1.15% | 0.90% | 0.90% |

All performance is still quoted net of fees.

- The Ongoing Charges Figure is based on the expenses incurred by the fund for the period ended 28th February 2026.

- Includes Investment Management Fee, Operational costs and look-through costs.

The figures may vary year to year

Fund Commentary - May 2026

The month oscillated between fears of a prolonged energy-driven stagflation (no growth coupled with inflation) shock and cautious optimism that the worst economic consequences of the Iran conflict may eventually be avoided. While the ceasefire that first came into effect in April broadly held throughout the period, the Strait of Hormuz remained closed, continuing to disrupt global energy markets and supply chains. Towards the end of the month, however, investors increasingly focused on the prospect of a negotiated settlement between the United States and Iran, with hopes growing that any eventual agreement could lead to the reopening of the strait and a gradual normalisation of trade flows.

Reflecting this backdrop, oil prices were highly volatile, rising when military tensions escalated and falling whenever progress towards a diplomatic solution appeared more likely. Although prices remained well above pre-conflict levels, they ended the month significantly below their highs as investor confidence grew that the disruption would not be permanent. The changing outlook for energy markets had a significant influence on inflation and interest-rate expectations. Earlier fears that a prolonged conflict would trigger a renewed inflation shock eased as energy prices retreated from their peaks. However, inflationary pressures already in the system started to emerge as higher energy costs filtered through supply chains into transportation, manufacturing and industrial inputs. The clearest evidence came in the United States, where producer-price inflation (the price at which goods are manufactured and sold to retailers) reached its highest level since 2022 and consumer inflation accelerated to a three-year high. Whilst hopeful that a negotiated settlement might be forthcoming, investors, particularly bond investors, remained alert to the possibility that a prolonged closure of Hormuz could eventually lead to genuine shortages rather than simply higher costs.

Interest-rate expectations moved lower over the course of the month but remained notably higher than they were before the conflict began, suggesting bond investors remain more sceptical than equity investors that the global economy can emerge unscathed from the crisis. At the start of the month, markets became increasingly concerned that central banks might need to tighten policy further in response to rising inflation. As hopes for a diplomatic resolution improved and oil prices moderated, those fears eased, particularly in the UK and Eurozone. By month-end, markets were pricing one fewer interest-rate increase than at the start of the month. However, stronger-than-expected US inflation data led investors to abandon expectations of a Federal Reserve (the US central bank) rate cut and instead price interest rates remaining unchanged. The Federal Reserve, European Central Bank and Bank of England all left rates on hold during the month. Economic data released over the month painted a mixed picture. Growth momentum weakened across several major economies as higher energy prices and uncertainty weighed on activity. US consumer sentiment softened, Chinese economic data disappointed, European growth remained subdued and UK labour-market conditions weakened amid rising political uncertainty following poor local election results for Labour and continued gains for Reform UK.

Financial markets nevertheless delivered strong returns. Equity investors increasingly looked beyond the immediate geopolitical risks and focused on resilient corporate earnings and continued investment in artificial intelligence. Technology and Asia-focused markets led gains, while Japanese equities were among the strongest-performing major markets globally. UK small and mid-sized companies also rebounded as fears of a prolonged energy shock receded. Bond markets recovered some ground towards month-end as inflation expectations moderated, although yields remained elevated and continued to reflect concerns around inflation, fiscal sustainability and geopolitical uncertainty. Sterling weakened against the US dollar, enhancing overseas returns for UK investors.

In May, the IFSL Wise Multi-Asset Income Fund rose 3.5%, slightly behind the IA Mixed Investment 40–85% Shares sector, which returned 3.8%. Given the strong performance of global risk assets, our equity holdings contributed positively to returns. Our UK equity funds, particularly those focused on small and mid-sized companies, Aberforth Smaller Companies and Odyssean Investment Trust, performed strongly, helped by the improved geopolitical backdrop, low starting valuations and continuing merger and acquisition activity that highlights overseas investors’ appetite for UK assets despite the unsettled political landscape. Our direct holding in Legal & General also performed well amid speculation that the company could become the subject of corporate activity. Within our international equity holdings, Pacific North of South EM Equity Income delivered strong performance, supported by several holdings benefiting from the AI theme.

Our strongest contributiona to performance came from our infrastructure holdings. The sector benefited from a decline in UK government bond yields as inflation concerns eased. Bond markets were also supported by comments from Andy Burnham, a potential future Labour leader, reaffirming a commitment to existing fiscal rules, helping to reassure investors over the UK’s fiscal outlook. Performance was further supported by positive company-specific developments. The Renewables Infrastructure Group reaffirmed its dividend targets, announced an expanded disposal programme, increased buyback capacity and reduced management fees, reinforcing confidence in the value of its underlying assets. Foresight Environmental Infrastructure delivered positive net asset value growth and highlighted the progress of its differentiated growth assets, which offer significant future value creation potential. HICL Infrastructure reported strong operational performance, completed asset disposals at premiums to carrying value, strengthened dividend cover and introduced governance reforms aimed at improving shareholder alignment. Our property holdings also announced positive operational updates from British Land, Helical and LondonMetric, the latter announcing a merger with Picton Property Income.

During the month, we initiated a position in VH Global Energy Infrastructure following the agreement of its wind-down strategy, which provides a clear catalyst for value realisation over the next two years. The portfolio offers a diversified collection of international infrastructure assets trading at a substantial discount to estimated realisable value, with relatively limited balance-sheet risk due to low levels of debt. This was funded through a reduction in Pantheon Infrastructure following strong performance and a significant narrowing of its discount to net asset value. We also increased our holdings in Prusik Asian Income and TwentyFour Strategic Income Fund.