Wise Multi-Asset Growth

Fund Ratings

Investment Objective

The investment objective of the Fund is to provide capital growth over Rolling Periods of 5 years in excess of the Cboe UK All Companies Index and in line with or in excess of the Consumer Price Index, in each case after charges.

Fund Attributes

- Aims to provide long term capital growth (over 5 year rolling periods) ahead of the Cboe UK All Companies Index and inflation.

- Specialised focus on investment trusts across asset classes.

- Adopts a value bias investment approach.

- Focus on high-quality funds and investment trusts investing in out-of- favour areas.

- Preference for fund managers with a disciplined, easy-to-understand investment process.

Investor Profile

- Seek capital growth over a long time frame.

- Accept the risks associated with the volatile nature of an adventurous multi-asset investment.

- Plan to hold their investment for the long term, 5 years or more.

Key Details

| Target Benchmark | Cboe UK All Companies, UK CPI |

|---|---|

| Comparator Benchmark (Sector) | IA Flexible Investment |

| Launch date | 1st April 2004 |

| Fund value | 69.5 million |

| Holdings | 41 |

| Valuation time | 12pm |

- Past performance is not a guide to the future

- Data as at 31st May 2026

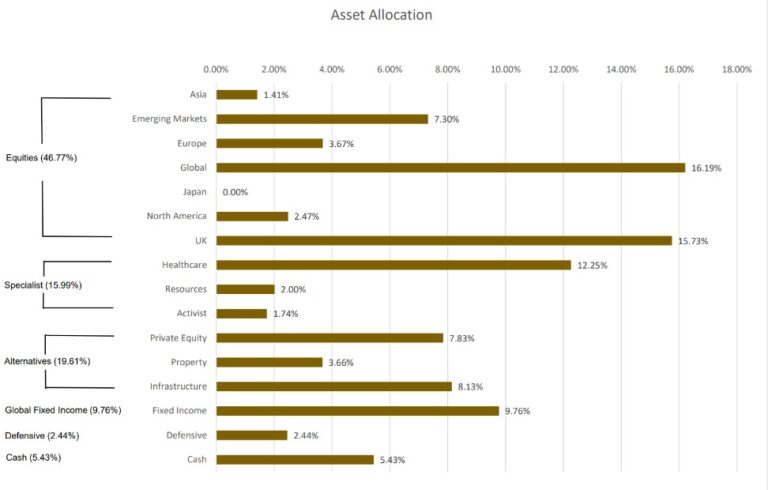

Investment Portfolio - May 2026

- Past performance is not a guide to the future

- Data as at 31st May 2026

Share Class Information

| | B Acc (Clean) | W Acc (Institutional) |

|---|---|---|

| Sedol Codes | 3427253 | BD386X6 |

| ISIN Codes | GB0034272533 | GB00BD386X65 |

| Minimum Lump Sum | £1,000 | £100 million |

| Initial Charge | 0% | 0% |

| IFA Legacy Trail Commission | Nil | Nil |

| Investment Management Fee | 0.75% | 0.50% |

| Operational Costs | 0.16% | 0.16% |

| Fund Management Costs | 0.23% | 0.23% |

| Ongoing Charges Figure 12 | 1.14% | 0.89% |

All performance is still quoted net of fees.

- The Ongoing Charges Figure is based on the expenses incurred by the fund for the period ended 28th February 2026.

- Includes Investment Management Fee, Operational costs and look-through costs.

The figures may vary year to year

Fund Commentary - May 2026

Unsurprisingly, the conflict in Iran continued to be the main driver of sentiment for financial markets in May, although it is notable that divergences between equity and bond markets persist. In terms of the war itself, despite regular announcements that an agreement between the US and Iran is very close, little has changed over the month. The ceasefire that first started on the 8th of April remains, broadly, in place notwithstanding some targeted attacks on both sides. However, critically, the Strait of Hormuz remains closed, thus continuing to impact global supply chains. While President Trump appears to be increasingly looking for a face-saving deal that would allow him to claim victory and, most importantly, allow for the re-opening of the strait, the Iranians are probably working to longer timeframes, unconstrained by democratic elections or much care for the suffering of their people. Having had a taste of the immense leverage they enjoy by holding the global supply chain hostage, they are unlikely to be under much pressure to accept punitive terms and will also want to claim victory. There was some hope that a meeting between Presidents Trump and Xi of China could provide an end to the impasse with the latter being a key business partner to Iran, but the Chinese seem content to let the US dig a bigger hole for themselves before any intervention.

As time passes, the impact on inflation of higher energy prices and other commodities such as fertilisers or critical manufacturing components is starting to be increasingly felt. The most striking evidence of this was the increase in the producer price index of more than 6% in the US, the highest since 2022. This measures the price inflation of products leaving factories, which reflects fluctuations in the cost of production of goods. It is then up to shops and distributors to decide how much of those fluctuations to pass on to the end consumers, as measured by the consumer price index. So far, the latter has been more measured but higher petrol prices are being felt too, with the consumer price index hitting a 3-year high in the US at 3.8%. The fear of rampant inflation hurting global economies if the conflict does not come to an end soon –thus creating actual shortages of commodities as opposed to the disruptions to supply chains currently being experienced-, is the main driver of higher bond yields on both sides of the Atlantic. In the US, the cost of borrowing for the US government over 30 years hit its highest level since the Great Financial Crisis of 2007-08. In the UK, similar borrowing costs hit their highest since 1998. The political instability in the UK following poor results in local elections for Labour, which is likely to trigger a leadership challenge and a move towards greater fiscal spending, is also unnerving bond investors.

We mentioned the divergences between equity and bond investors’ sentiment in introduction, however, and the contrasts are sharp. While bond markets reflect a fear that the war will be prolonged, equities continue to price in a much more benign environment with all major equity markets in the black in May, many of them at or close to their all-time highs. The volatility index in the US (a common measure of investor fear) is lower than it was before the conflict began at the end of February. Even oil, which should be at the forefront of investor concerns, is about 25% lower than its March high, itself lower than during the invasion of Ukraine by Russia, despite the volume of oil and gas impacted by the closure of the Strait of Hormuz being a multiple of what it was at that time. Risk investors thus seem willing to price in a resolution of the war in the short-term, which may or may not be the case, but the risks appear skewed to the downside in the event of any disappointment. In terms of company results, however, it is undeniable that corporates, particularly in the US but also in Asia, continue to fire on all cylinders with Q1 earnings growing at the fastest rate in 5 years, predominantly driven by the AI boom. Anticipated IPOs (Initial Public Offerings when private companies open their capital up to trade on a stock exchange) from behemoths like SpaceX, OpenAI and Anthropic also help keep equity investors perky.

In May, the IFSL Wise Multi-Asset Growth Fund rose 3.6%, ahead of the CBOE UK All Companies Index (+0.9%) but behind its peer group, the IA Flexible Investment sector (+4.3%). The top contributors to performance were found in UK smaller companies, specifically Odyssean and Aberforth Smaller Companies supported by strong trading updates and M&A (Merger and Acquisition) speculation from a number of their holdings, as well as some noticeable insider share purchases (i.e. when an executive of the company buys shares) which tend to be a good indication of the conviction of management in their stocks. In emerging markets, both Mobius and Templeton Emerging Markets had a strong month supported by buoyant markets in South Korea and Taiwan where semiconductor-related companies are prized by investors. Finally, it is worth noting the strong performance of RIT Capital as investors are starting to realise the upside potential from its private holdings, including Space X, Open AI and Anthropic mentioned earlier. All three of those are preparing for an IPO in the next few months and have seen sharp revaluations upwards recently following new capital raises. RIT only revalue their private holdings twice a year and these companies are held at their 2025 valuations in the trust, thus materially below their current valuations. On the negative side, only Fidelity China Special Situations and our two listed equities infrastructure funds were marginal detractors.

From a portfolio perspective, while acknowledging the fundamental strength at the corporate level, we want to maintain some powder dry in case the benign geopolitical scenario favoured by equity investors gets derailed. We thus trimmed strong performers such as Templeton Emerging Markets and Mobius Investment Trust. We also reduced our position in Achilles Investment Company following some positive M&A news on its holding in Spire Healthcare. This raised our cash to 5.4%. We also rotated some of our holding in Pantheon International, a standout performer in the listed private equity sector for the past few months, into Oakley Capital.