For Professional Clients Only

Macro & Market Update

US tariffs once again made headlines in February following the US Supreme Court ruling that presidents lack legal authority to impose sweeping tariffs, clarifying that this authority belongs to Congress and rendering the tariffs imposed by President Trump last April illegal. Following a Federal Reserve (the US central bank) report that about 90% of tariffs last year were borne by American businesses and consumers through higher end prices rather than by foreign companies, the ruling itself could be perceived as the equivalent of striking down a government for implementing an illegal consumption tax. The Supreme Court did not rule on the question of refunds, however, opening the door to further litigation. Meanwhile, immediately after the Supreme Court ruling, President Trump announced a new temporary blanket global tariff of 10%, valid for a maximum of 150 days during which the administration will no doubt look for a legal way to tax imports. This new regime throws trade deals agreed in the past few months into question with some countries, including the UK and the EU, ending worse off despite making hard concessions to the US than counterparts such as Brazil and China, which have so far resisted pressure from Trump. For now, investors have broadly taken this new bout of uncertainty in their stride, with volatility a long way from the highs reached last year post-“liberation day”.

Another important development in February was the landslide victory of Sanae Takaichi in the snap general election in Japan. Despite some concerns about the viability of her fiscal stimulus and tax cutting plans, investor sentiment is supported by the prospect of a stable pro-growth government. The same cannot be said about the UK government where the lack of economic direction and indecisiveness is putting Prime Minister Starmer’s position in jeopardy. The British economy grew at an anaemic 0.1% in Q4 but inflation fell more than expected to 3% opening the door for more rate cuts from the Bank of England, although no change occurred last month. By contrast, in the US, the Federal Reserve remains wary of recent progress made on inflation and, with strong employment figures last month, indicated that they remain firmly on hold. Some weakness is starting to appear in the US, however, mainly observable in weaker consumer confidence, partly contributing to economic growth slowing to 1.4% in Q4 versus 2.8% in Q3. On the last day of the month, geopolitical tensions overtook economic concerns with the US launching an attack on Iran and the conflict spreading across the region.

In markets, the key development was weakness in technology companies, especially in software. Over recent weeks, investors have been worrying about the scale of expenditure plans from big tech companies on AI-related projects, such as data centres. While most of this spending can be financed by corporate cashflows, the increasing use of debt is causing concerns about overspending in a technology that is yet to prove it can be monetized. As a result, all the so-called Magnificent Seven companies (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) are trading below their peaks, some of which were reached as far back as three months ago. While there are concerns about overspending and whether AI will meet the lofty growth expectations already priced in, there are also worries about how AI will disrupt adjacent businesses. Announcements of breakthroughs from a few AI developers in sectors such as legal, tax and accounting services, and wealth management caused a sharp decline in software companies. The fear is that corporate clients of these software companies will soon be able to pay a fraction of their subscription cost to an AI agent for equivalent results, potentially rendering incumbent service providers redundant. For now, markets are neither willing nor able to discern between winners and losers in the AI revolution causing global software companies to fall by 20% year-to-date.

Fund Performance

Wise Multi-Asset Growth

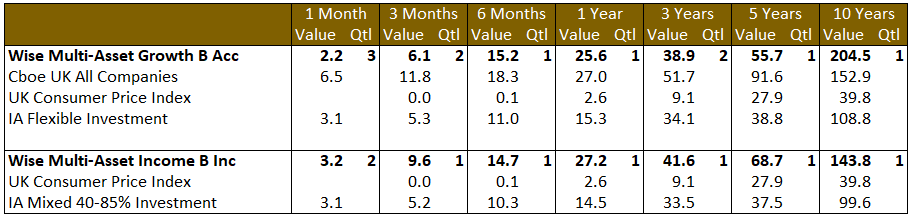

In February, the IFSL Wise Multi-Asset Growth Fund was up 2.2%, behind the CBOE UK All Companies Index (+6.5%) and its peer group, the IA Flexible Investment sector (+3.1%). The strength in the UK index was driven by the oil and mining sector, as well as the global rotation away from technology into asset-heavy companies (i.e. out of the new economy and into the old). Our Fund benefitted from these themes too with our strongest contributors being Ecofin Global Utilities and Infrastructure, and Premier Miton Global Infrastructure Income. Another top contributor was TR Property, with AI unlikely to affect the property sector much. Our bias towards value managers across developed and emerging regions also helped thanks to exposure away from highly valued tech and into those sectors that have been neglected for years. The negative contributors were our private equity names with many players in the sector heavily exposed to software, thanks to their recurring revenues and the scalability of these businesses. Our managers in that space are not immune with on average about a third of their respective portfolios exposed to technology. We believe, however, that they can pick the winners in that space and, the discounts of ~30% at which they trade should provide some margin of safety, even if volatility is unlikely to recede quickly. Our position in Pershing Square, our only US equity manager, also suffered from its exposure to some of the Magnificent Seven companies but we take comfort from the fact that these positions were acquired on previous periods of weakness and that the trust itself trades on a 25% discount for what is a portfolio of very liquid positions.

Wise Multi-Asset Income

In February, the IFSL Wise Multi-Asset Income Fund rose 3.2%, ahead of the IA Mixed Investment 40–85% sector, which gained 3.1%. February marks the end of the financial year of the fund over which time the fund has risen 27.2%, ahead of the peer group which rose 14.5%. The distribution per unit for the B Income share class has risen 10% (final dividend to be confirmed). Over the course of the year, we have rotated the exposure of the fund towards more defensive, higher yielding holdings which should see continued strong growth in the distribution. For the year ahead, we currently forecast a yield on the fund of 4.9%, which should provide a solid foundation to future performance over the medium term. Over the month, our infrastructure holdings were the strongest contributors to returns helped by falling government bond yields and a recognition that a key constraint to the pace of the rollout of AI capital expenditure plans will be power generation and electricity grid capacity. HICL Infrastructure, Ecofin Global Utilities and Infrastructure and International Public Partnerships were strong performers as was Bluefield Solar Income, where expectations that the formal sale process for the company remains on track. February saw strong performance from equity markets outside the US as investors continued to rotate towards less expensive, less technology dominated international markets. Our UK, Canadian, Emerging Market and Global Value equity holdings all performed strongly. Our commodity holdings also performed very strongly as gold rebounded following a sharp fall last month on the appointment of the next Chairman of the Federal Reserve whilst oil prices rose as tensions over Iran mounted. Our property holdings also performed well with Picton Property Income confirming takeover interest from LondonMetric whilst Helical announced funding for its Paddington development and the profitable forward sale of a student housing development. Our Private Equity holdings were the major detractors over the month as concerns around their software holdings led to discount widening.

All data is in a total return format

Past performance is not a guide to future performance

Portfolio Changes

Wise Multi-Asset Growth

In terms of portfolio activity, we remain disciplined in taking profit and have done so in Ecofin Global Utilities and Infrastructure, Premier Miton Global Infrastructure Income, Jupiter Gold & Silver and Templeton Emerging Markets. We used some of the cash accumulated in recent weeks to take a new position in HG Capital Trust, the largest investor in private technology companies in Europe, which we used to own until the end of 2020 when valuations got too expensive for us. After a close to 30% fall over a week and with the discount widening to levels rarely seen in its 31-year history, we took the opportunity to start rebuilding a position. Whilst mainstream investors woke up to the AI threat only recently, the team at HG have been working with their underlying companies for years to develop and integrate their own AI capabilities and moats, which should put them on a strong footing for the challenges ahead. It will surely take time for investors to get convinced this is indeed the case, so we have only taken a starter position for now but believe that this will be an attractive entry point for patient investors.

Wise Multi-Asset Income

Over the month, we continued to reduce our commodity exposure given the strength of recent performance. Similarly, we reduced our holding in Ecofin Golbal Utilities and Infrastructure. We added to our renewables holdings, Foresight Environmental Infrastructure and Renewables Infrastructure Group as well as increasing our equity holdings in Prusik Asian Equity Income, Man Income Fund and Brickwood Global Value. Our cash position remains relatively high at over 5%.

TO LEARN MORE ABOUT THESE FUNDS, PLEASE CONTACT

01608 695 180 OR EMAIL JOHN.NEWTON@WISE-FUNDS.CO.UK

WWW.WISE-FUNDS.CO.UK

Full details of the IFSL Wise Funds, including risk warnings, are published in the IFSL Wise Funds Prospectus, the IFSL Wise Supplementary Information Document (SID) and the IFSL Wise Key Investor Information Documents (KIIDs) which are available on request and at wise-funds.co.uk/our funds. The IFSL Wise Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. Capital appreciation in the early years will be adversely affected by the impact of initial charges and you should therefore regard your investment as medium to long term. Every effort is taken to ensure the accuracy of the data used in this document but no warranties are given. Wise Funds Limited is authorised and regulated by the Financial Conduct Authority, No768269. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.