Wise Multi-Asset Growth

Fund Ratings

Investment Objective

The investment objective of the Fund is to provide capital growth over Rolling Periods of 5 years in excess of the Cboe UK All Companies Index and in line with or in excess of the Consumer Price Index, in each case after charges.

Fund Attributes

- Aims to provide long term capital growth (over 5 year rolling periods) ahead of the Cboe UK All Companies Index and inflation.

- Specialised focus on investment trusts across asset classes.

- Adopts a value bias investment approach.

- Focus on high-quality funds and investment trusts investing in out-of- favour areas.

- Preference for fund managers with a disciplined, easy-to-understand investment process.

Investor Profile

- Seek capital growth over a long time frame.

- Accept the risks associated with the volatile nature of an adventurous multi-asset investment.

- Plan to hold their investment for the long term, 5 years or more.

Key Details

| Target Benchmark | Cboe UK All Companies, UK CPI |

|---|---|

| Comparator Benchmark (Sector) | IA Flexible Investment |

| Launch date | 1st April 2004 |

| Fund value | 70.0 million |

| Holdings | 41 |

| Valuation time | 12pm |

- Past performance is not a guide to the future

- Data as at 31st July 2026

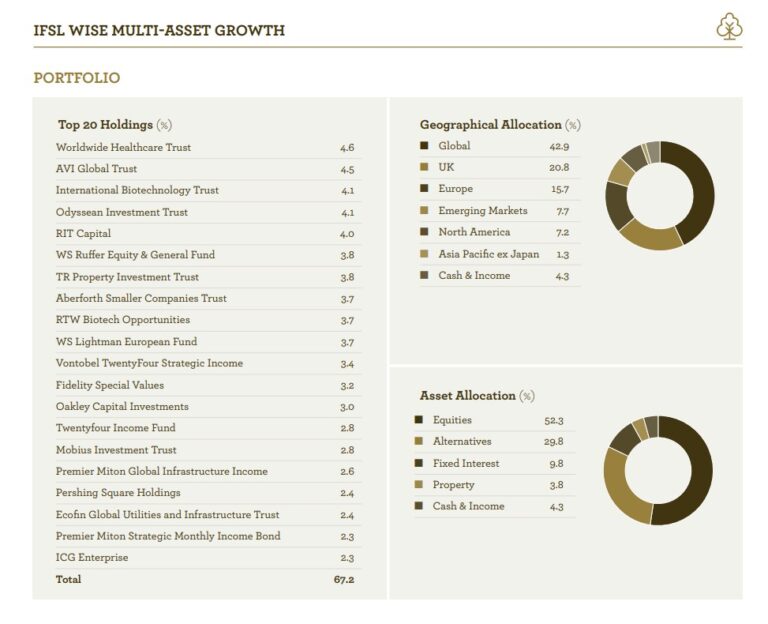

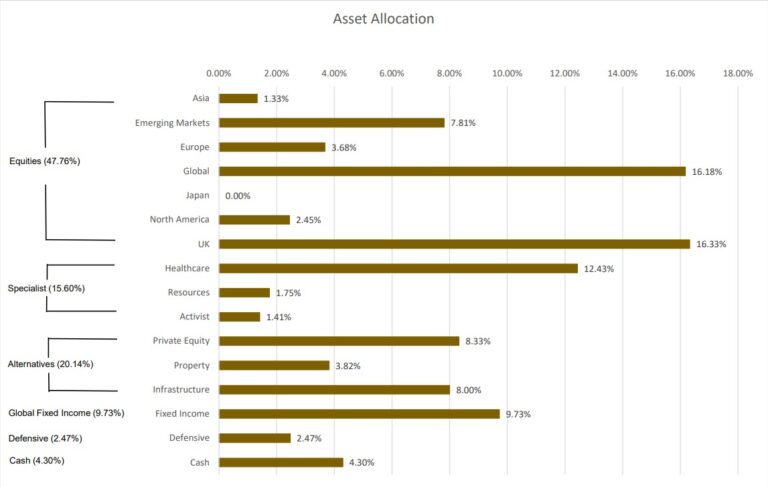

Investment Portfolio - July 2026

- Past performance is not a guide to the future

- Data as at 31st July 2026

Share Class Information

| | B Acc (Clean) | W Acc (Institutional) |

|---|---|---|

| Sedol Codes | 3427253 | BD386X6 |

| ISIN Codes | GB0034272533 | GB00BD386X65 |

| Minimum Lump Sum | £1,000 | £100 million |

| Initial Charge | 0% | 0% |

| IFA Legacy Trail Commission | Nil | Nil |

| Investment Management Fee | 0.75% | 0.50% |

| Operational Costs | 0.16% | 0.16% |

| Fund Management Costs | 0.23% | 0.23% |

| Ongoing Charges Figure 12 | 1.14% | 0.89% |

All performance is still quoted net of fees.

- The Ongoing Charges Figure is based on the expenses incurred by the fund for the period ended 28th February 2026.

- Includes Investment Management Fee, Operational costs and look-through costs.

The figures may vary year to year

Fund Commentary - July 2026

Market movements took precedence over macroeconomic developments in July as the nervousness around AI trades that started brewing in June snowballed to create a high level of volatility. As we mentioned in last month’s commentary, there have been growing concerns about the amount of money spent by hyperscalers such as Alphabet, Amazon, Meta and Microsoft on data centres because of the lack of visibility on future returns on capital. The AI revolution is real, but nobody can yet predict who the winners will be, how it will be monetized nor how much computing power it will require. As such, while it is understandable that large technology companies try to ensure they stay in the race (particularly given the vast amount of cash available to them), it is equally understandable that investors finally question how they will get their money back.

The Nasdaq index, a bellwether in the US for technology companies, entered a correction in July as a result (the term used to describe a 10% drop from the most recent peak). Until recently, however, chip manufacturers such as Nvidia in the US or Samsung and SK Hynix in South Korea were seen as the better way to play the AI theme. Irrespective of which AI model wins the race, all of them need a huge amount of computing power and semiconductors are necessary to achieve it. Thanks to huge order books providing these companies with visibility in revenues for the next few years, a lot of investors have flocked into their shares to generate extraordinary returns. As an illustration, SK Hynix went up about 900% in the year to the end of June 2026. The company went on to fall close to 60% at its worst in July, however, on the back of disappointing results. This shows how, when investors’ expectations become disconnected from reality and momentum takes a life of its own, risks get amplified. This is not to say we are at the stage where the bubble bursts yet, and such moves are often part of price patterns during periods of exuberance. Volatility of this sort has to be factored into the latter stages of a strong market like we are in now, however. Given how dominant the AI theme has been for months, movements of that magnitude certainly are noticeable, but it is encouraging to see that non-tech-related stocks generally performed strongly, helped by more attractive valuations and an acceleration in corporate activity (mergers and acquisitions), which led to a rotation towards less expensive names.

Bonds were also volatile in July, driven by higher oil prices -and thus fear of inflation and higher interest rates, but also by poor communication from the US central bank (or Fed). Oil prices went from $70 a barrel at the start of the month to $105 when the ceasefire in the Strait of Hormuz came to an end and tit-for-tat attacks between Iran and the US took place over a number of days. It ended the month lower at $87. The ceasefire was always fragile given the lack of trust between both parties, but it is now unclear how the strait can sustainably reopen in the short term. While inflation in both the US and the UK surprisingly came down and no central bank increased rates over the month, higher energy prices put bond investors on the defensive. Moreover, the new Chair of the Fed, Kevin Warsh, is intent on stopping guidance to market participants with the view that markets should price in data and react to it, rather than pricing in how they think the Fed will react to the data. As he put it, he wants “market participants to learn to play the ball, not the referee”. This certainly has merits and it can easily be argued that investors have got too hung up on every word, punctuation and omission from central bankers’ speeches, but markets still need to have an inkling about how strict or lenient the referee will be so they can adjust their play. This uncertainty sent the 30-year US bond yields to their highest level since 2007, impacting cost of borrowing, and it seems that Warsh will need to improve and polish his communication skills going forward to avoid losing credibility and control of the bond market.

In other news, Trump found a new way to impose tariffs of at least 10% on 60 countries, including the UK, EU and Japan, after his first attempt on “Liberation Day” last year was ruled illegal. This new tool is linking tariffs to the alleged failure of those countries to enforce the prohibition on importation of goods produced with forced labour, a relatively obscure rule used with little evidence of wrongdoing from the recipients which will surely trigger reciprocal measures and continue to disturb global trade and relationships. Finally, China’s domestic consumption and investment woes came through in their latest GDP growth figure, at its lowest level since at least the early 1990s, coming in at 4.3% per annum, below its 4.5-5% target announced for 2026.

In July, the IFSL Wise Multi-Asset Growth Fund rose 2.2%, behind the CBOE UK All Companies Index (+3.9%) but ahead of its peer group, the IA Flexible Investment sector (-0.7%). The main contributor was RIT Capital Partners which benefitted from the SpaceX listing, forcing a revaluation of its holding last valued in December 2025 (private holdings are usually only revalued twice a year). It also announced a tender offer (a proposal by the company to buy a set number of shares from shareholders) which pushed the discount sharply tighter. Our UK equity funds also performed strongly, helped by accelerating merger and acquisition activity, including for Odyssean with a bid at a 41% premium for one of their top holdings. Finsbury Growth and Income also benefitted from strong earnings reports from holdings Sage and RELX helping to put fears of AI cannibalisation at bay, as well as Unilever and Burberry. In Private Equity, Oakley Capital recovered its losses from June. On the negative side, Mobius and Templeton in emerging markets gave some of their recent strong gains back, as did International Biotechnology Trust.

In terms of portfolio activity, we took some profits in RIT Capital Partners, Odyssean, Pacific North of South Emerging Equity Income, RTW Biotech Opportunities and Aberforth Smaller Companies. We also reduced our holding in Achilles Investment Company. We used those proceeds to top up Neuberger Berman Emerging Markets Fund, Finsbury Growth & Income, Pershing Square and AVI Global. Our cash levels remained on the cautious side at 4.3%.