For Professional Clients Only

Macro & Market Update

The war in Iran continued to dominate market narratives in April, although investor sentiment about a relatively quick resolution to the conflict was far more sanguine than it had been a few weeks earlier. The month was a roller-coaster of announcements from both the US and Iran, aimed at domestic audiences while also sending public messages as a negotiating tactic, which created confusion and uncertainty. By the end of April, military attacks had largely stopped following a ceasefire first agreed on 8th April for an initial two-week period and subsequently extended to allow talks to take place. A first round involving Vice President Vance proved unsuccessful, while a second round later in the month was indefinitely postponed. Although the conflict is far from over, market participants have interpreted the ceasefire and negotiations as signs that both President Trump and the Iranians are starting to feel the costs of the war and are looking for a face-saving way to end it while still claiming victory. Meanwhile, although bombings may have stopped, the Strait of Hormuz remains closed and the impact on energy, food, fertilisers, and critical manufacturing components is increasingly being felt globally. Long transportation times and some supply-chain flexibility mean that the physical impacts of the war outside the region take time to become apparent; however, the longer the strait remains closed, the more evident global dependence on Gulf commodities will become.

On the economic front, inflation is the most obvious data point affected by the conflict, with oil and gas markets rising sharply since the beginning of March. Inflation came in at 2.5% (up from 1.9%) in the Eurozone at the end of March, followed by 3.3% in both the US (vs 2.4%) and the UK (vs 3.0%). Excluding energy and food, so-called core inflation has broadly remained stable; however, higher energy costs and shortages will eventually feed through to consumer prices if the situation is prolonged. As an illustration, Chinese producer prices rose in April for the first time since 2022. Growth, by contrast, has so far been relatively unaffected, although it surprised to the downside in the US on the last day of the month (2.0% annualised in Q1 vs 2.2% expected). The International Monetary Fund (IMF) updated its growth forecasts to reflect the war in Iran, cutting expectations globally. Among developed countries, the largest downgrade was for the UK, reduced from 1.3% to 0.8% for full-year 2026 due to the UK’s heavy dependence on global energy markets. The risk of recession cannot be excluded in the event of further escalation, but investors generally brushed off these fears. Equity markets performed strongly in April, with US and Asian markets notably back to their pre-war levels. Meanwhile, bond markets priced in a higher likelihood of rate hikes (to combat inflation) than rate cuts (to support growth), except in the US, where political pressure from President Trump to cut rates adds a non-economic dimension to the central bank decision. In the last week of the month, central banks in Japan, the US, the UK, and the Eurozone kept rates unchanged and reiterated their base case that inflation will be transitory, while highlighting upside risks to price pressures. Finally, in the UK, political uncertainty with regards to the Prime Minister’s position also contributed to pushing bond yields higher due to fiscal concerns.

Away from macro developments, the mergers and acquisitions (M&A) market continued to build on the strong momentum that began last year, supporting equity investor sentiment, with more than $1.2 trillion of deals announced in the first quarter. This was a record and the third consecutive quarter with more than $1 trillion of announced deals. Earnings also remained supportive, particularly in the US, where Q1 results are expected to be the strongest since 2021, thanks to AI-related themes continuing to be the main driver. This helped large technology companies recover in April, with top index names Nvidia, Alphabet, and Amazon surpassing their previous highs from last November.

Fund Performance

Wise Multi-Asset Growth

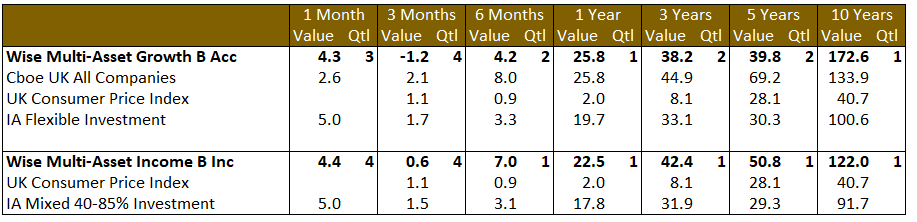

In April, the IFSL Wise Multi-Asset Growth Fund rose 4.3%, ahead of the CBOE UK All Companies Index (+2.6%) but behind its peer group, the IA Flexible Investment sector (+5%). This brought performance back into positive territory for the year (+1.1%) and left it flat since the start of the conflict in Iran. Contributors were varied but, unsurprisingly given the recovery in risk appetite during the month, came predominantly from equity funds, particularly those that struggled in the immediate aftermath of the US/Israeli attacks on Iran. Small UK companies performed well, not only as a recovery trade but also thanks to M&A activity, which continued apace. This benefited Odyssean, as well as Amati UK Smaller Companies. M&A also remained a key driver of performance in the biotechnology sector, with International Biotechnology seeing two further positions (including its largest) taken over at premiums of around 35% each. RTW Biotech Opportunities also benefited from the IPO (Initial Public Offering, i.e. when a private company lists on a stock exchange) of Kailera Therapeutics, one of the most promising obesity drug developers. After its first day of trading, the company’s share price was 139% higher than the end-March valuation used in the RTW portfolio. This outcome is particularly pleasing because it illustrates the managers’ full life-cycle investing approach by which they help launch a company from scratch, support it with funding and resources during development, take it public, and remain a cornerstone investor to fully realise the benefits of their investment. Mobius Investment also performed strongly, supported by robust emerging markets, particularly in the semiconductor sector. Finally, Ecofin Global Utilities and Infrastructure saw its discount tighten sharply, helped by its positioning in a sweet spot between defensive utilities and beneficiaries of the push to increase electricity production to meet AI-driven demand.

Wise Multi-Asset Income

In April, the IFSL Wise Multi-Asset Income Fund rose 4.4%, slightly behind the IA Mixed Investment 40–85% sector, which returned 5%. Performance was driven by a broad-based rebound in risk assets as the geopolitical backdrop shifted from active conflict towards ceasefire and negotiation. This improvement in sentiment particularly benefited those areas that had been weakest in the prior month, with equities, property and infrastructure leading the gains. Equity markets were a key contributor, with strength particularly evident across our UK holdings. Odyssean Investment Trust performed strongly, supported by a takeover bid for Blackline Safety and a robust trading update from XP Power, its largest holding. More broadly, value-oriented UK strategies benefited from improving sentiment towards domestically exposed businesses. International Biotechnology Trust was again notably strong, benefiting from two more bids for holdings within its portfolio. Elsewhere, holdings that were sold off last month, such as BlackRock World Mining Trust and Pacific North of South EM Equity Income Opportunities, rebounded strongly. Property also recovered meaningfully. This was helped by a series of reassuring company updates highlighting that demand for high-quality assets remains resilient. British Land reported strong leasing activity and rental growth, particularly in prime London campuses benefiting from demand linked to technology and AI-related occupiers. Helical continued to make progress in leasing and development, reducing risk across its pipeline and improving visibility on future income. Meanwhile, LondonMetric delivered stable income growth supported by high occupancy and long lease structures. These updates reinforced confidence that well-located, high-quality real estate continues to perform even in a more uncertain macro environment.

Infrastructure and renewables also contributed positively. Holdings such as The Renewables Infrastructure Group and Foresight Environmental Infrastructure performed well as concerns around government intervention to counter higher power prices proved less severe than initially feared. Policy changes introduced during the month were aimed at lowering electricity prices, reducing volatility, and weakening the link between power prices and gas prices. In simple terms, the government is seeking to move towards a system where renewable generators receive more stable, fixed pricing for their output. While this may limit upside in extreme pricing environments, it improves the predictability of cashflows, with only limited impact on net asset values and potential longer-term benefits through lower discount rates.

All data is in a total return format**

Past performance is not a guide to future performance

Portfolio Changes

Wise Multi-Asset Growth

From a portfolio perspective, we maintained a balanced approach, recognising geopolitical risks while also acknowledging pockets of fundamental strength. We therefore took some profits in our strongest performers, including Odyssean, Ecofin Global Utilities and Infrastructure, BlackRock World Mining, and Pantheon International. Conversely, we topped up relative underperformers such as Fidelity Special Values, Finsbury Growth & Income, Aberforth Smaller Companies, Man Undervalued Assets, and ICG Enterprise. At month-end, we also made a new investment in the Neuberger Berman Emerging Markets Equity fund, a newly launched strategy managed by the former Schroders Emerging Markets team, whose departure last autumn had forced us to exit the fund at the time. As in their previous vehicle, this is a differentiated value strategy in emerging markets and is particularly attractive at present given the sharp discrepancies across the region between expensive parts of the market (typically linked to semiconductors and technology) and more cheaply valued areas.

Wise Multi-Asset Income

Over the month, we recycled capital by trimming positions that had performed strongly since the start of the Iran conflict and year to date, including Pantheon Infrastructure, Middlefield Canadian Enhanced Income, Odyssean Investment Trust and Ecofin Global Utilities and Infrastructure. We selectively added to equity positions such as Fidelity Special Values, Finsbury Growth & Income and Brickwood Global Value, where performance had lagged. We also maintained portfolio balance by adding to fixed income and property exposures, while rebalancing renewables. Finally, we initiated a position in the Neuberger Berman Emerging Markets Equity fund, a differentiated value strategy managed by the former Schroders Emerging Markets team, which we believe is well positioned given the current valuation dispersion across emerging markets.

** Performance data has used IFSL Wise Multi-Asset Income B Acc share class due to an issue with FE data

TO LEARN MORE ABOUT THESE FUNDS, PLEASE CONTACT

01608 695 180 OR EMAIL JOHN.NEWTON@WISE-FUNDS.CO.UK

WWW.WISE-FUNDS.CO.UK

Full details of the IFSL Wise Funds, including risk warnings, are published in the IFSL Wise Funds Prospectus, the IFSL Wise Supplementary Information Document (SID) and the IFSL Wise Key Investor Information Documents (KIIDs) which are available on request and at wise-funds.co.uk/our funds. The IFSL Wise Funds are subject to normal stock market fluctuations and other risks inherent in such investments. The value of your investment and the income derived from it can go down as well as up, and you may not get back the money you invested. Capital appreciation in the early years will be adversely affected by the impact of initial charges and you should therefore regard your investment as medium to long term. Every effort is taken to ensure the accuracy of the data used in this document but no warranties are given. Wise Funds Limited is authorised and regulated by the Financial Conduct Authority, No768269. Investment Fund Services Limited is authorised and regulated by the Financial Conduct Authority, No. 464193.