Wise Multi-Asset Growth

Fund Ratings

Investment Objective

The investment objective of the Fund is to provide capital growth over Rolling Periods of 5 years in excess of the Cboe UK All Companies Index and in line with or in excess of the Consumer Price Index, in each case after charges.

Fund Attributes

- Aims to provide long term capital growth (over 5 year rolling periods) ahead of the Cboe UK All Companies Index and inflation.

- Specialised focus on investment trusts across asset classes.

- Adopts a value bias investment approach.

- Focus on high-quality funds and investment trusts investing in out-of- favour areas.

- Preference for fund managers with a disciplined, easy-to-understand investment process.

Investor Profile

- Seek capital growth over a long time frame.

- Accept the risks associated with the volatile nature of an adventurous multi-asset investment.

- Plan to hold their investment for the long term, 5 years or more.

Key Details

| Target Benchmark | Cboe UK All Companies, UK CPI |

|---|---|

| Comparator Benchmark (Sector) | IA Flexible Investment |

| Launch date | 1st April 2004 |

| Fund value | 69.2 million |

| Holdings | 41 |

| Valuation time | 12pm |

- Past performance is not a guide to the future

- Data as at 30th June 2026

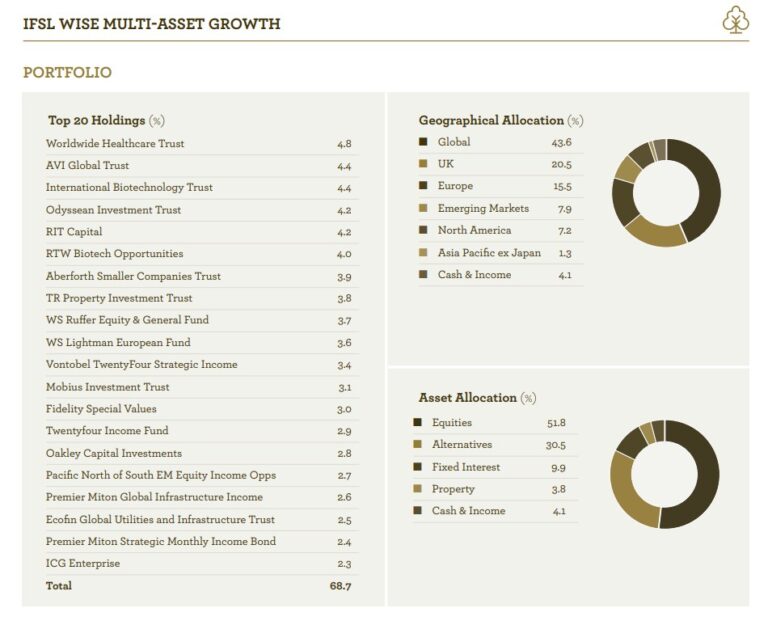

Investment Portfolio - June 2026

- Past performance is not a guide to the future

- Data as at 30th June 2026

Share Class Information

| | B Acc (Clean) | W Acc (Institutional) |

|---|---|---|

| Sedol Codes | 3427253 | BD386X6 |

| ISIN Codes | GB0034272533 | GB00BD386X65 |

| Minimum Lump Sum | £1,000 | £100 million |

| Initial Charge | 0% | 0% |

| IFA Legacy Trail Commission | Nil | Nil |

| Investment Management Fee | 0.75% | 0.50% |

| Operational Costs | 0.16% | 0.16% |

| Fund Management Costs | 0.23% | 0.23% |

| Ongoing Charges Figure 12 | 1.14% | 0.89% |

All performance is still quoted net of fees.

- The Ongoing Charges Figure is based on the expenses incurred by the fund for the period ended 28th February 2026.

- Includes Investment Management Fee, Operational costs and look-through costs.

The figures may vary year to year

Fund Commentary - June 2026

It was a volatile month for financial markets in June. Although the month started with ongoing strikes and tensions between the US/Israel and Iran, a temporary deal was eventually agreed between the two sides allowing negotiations towards more permanent arrangements to take place within a 60-day ceasefire framework. Crucially, the memorandum of understanding (MoU) between the US and Iran agreed the immediate re-opening of the Strait of Hormuz which helped Brent crude oil drop from about $100 a barrel down to $70 over the period. As has been the case since the conflict began, however, while a definite improvement and a great step forward, it is too early to call the end of the war for good. The MoU is not equivalent to a peace deal and lacks detail. Also, both sides lack trust in each other and fire continued to be exchanged later in the month despite the ceasefire. The Iranian regime accepted the deal in order to receive an immediate financial boost by being allowed to sell its oil again, while President Trump is under increasing pressure to turn the page on a war of choice that is diminishing his authority within his own party, as well as threatening his legacy.

Despite some necessary caution, the above was undeniably good news for investors, but the moderate market reaction highlighted that this was already priced in after a strong period of performance for equities since the beginning of April, illustrating the adage that it often is better to travel than to arrive. The reaction was more positive in bond markets where inflation fears from higher energy prices had driven yields higher in longer-dated bonds (10+ years). The deal with Iran relieved some of that pressure. At the shorter-end, rather than inflation per se, it is central banks’ interest rate decisions that tend to drive bond yields, and we saw some diverging reactions between regions in June. The European Central Bank was the first one to hike rates due to inflationary pressures on energy prices from the war, its first since mid-2023, although it was in line with market expectations. The Bank of Japan also hiked but has been on a different interest rate path from other developed economies for years. The Bank of England (BoE) kept its base rate unchanged, helped by a surprise steady inflation reading of 2.8% last month. Although this is expected to only be a temporary reprieve, the BoE is hoping that it will not have to put on the brakes to combat inflation while growth in the UK remains weak. It will also keep a close eye on the plans from the new leader of the Labour Party over the next few weeks, following the resignation of Prime Minister Starmer. The US central bank (the Federal Reserve or Fed) was the most significant for markets, despite keeping its rate unchanged. It was the first meeting of Chair Warsh, appointed by Trump and under explicit pressure from the President to lower interest rates. With inflation during the month coming in at 4.2% vs 2.4% prior to the Iran war, with stronger than expected employment numbers in June, and with strong retail sales, Warsh and the Fed committee instead strongly hinted at a readiness to hike rates over the next few months. As such, bond investors went from pricing in no rate hike this year to one hike by December.

This change in interest rate expectations in the US put the most growth-oriented part of the equity market (the names reliant on future earnings to justify their current valuations) under pressure. At the same time, we are clearly starting to see increasing questioning from investors about the future profitability of the gigantic spending in AI-related projects. Capital expenditure from the largest hyperscale tech companies went from $412bn in 2025 to an estimated $754bn in 2026 and $905bn in 2027 according to Goldman Sachs. Increasingly, rather than relying on their own cashflows, these hyperscalers are raising capital from both equity and bond markets and the pricing of these raises suggests that investors are less willing to write them blank checks. As a result, an equally-weighted basket of the Magnificent 7 (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) fell more than 14% peak-to-trough in June. Even the largest company listing in history, Space X, dropped by a third after its first week of trading. That said, the AI trade remains alive and well, but it is the “picks and shovels” names like semiconductor manufacturers that are now favoured over the AI model developers. A final related point worth keeping an eye on for equity markets is when all this capital raising will run out of buyers. 2026 will be the first year since 2003 when more US shares are issued than bought back from companies. The former era provided a huge boost to equity valuations, but this may be slowly changing.

In June, the IFSL Wise Multi-Asset Growth Fund rose 0.3%, behind the CBOE UK All Companies Index (+0.5%) but in line with its peer group, the IA Flexible Investment sector (+0.3%). We have purposedly avoided direct AI trades because we cannot make sense of valuations. AI affects most sectors, however, from infrastructure to commodities, or from financials to biotechnology to name but a few. We also have exposure to AI themes via heavily discounted investment trusts (e.g. private equity, infrastructure, value equity), giving us sufficient margin of safety to participate on the upside. Some of those had a difficult month in June, like Pershing Square which has built exposure to some Magnificent 7 companies recently on weakness, or Oakley Capital which has exposure to technology companies. Meanwhile, the competition for capital driven by some of the new equity issuances mentioned above, drained capital from other parts of the market, like precious metals for example, impacting Jupiter Gold & Silver and Blackrock World Mining. Finally, AVI Global had a difficult month driven by stock-specific weaknesses as well as some profit taking in Korea.

On the positive side, our biotechnology names continued to benefit from acquisitions of their holdings by large pharmaceutical companies. Our infrastructure basket also contributed positively, supported by lower long-term bond yields. Finally, in emerging markets, Mobius Investment Trust continued its strong run since the start of the quarter.

In terms of portfolio activity, we trimmed strong performers International Biotechnology Trust and Foresight Environmental Infrastructure. We redeployed the proceeds, as well as some of the cash we had accumulated in recent weeks, into what we think are attractively valued opportunities: Neuberger Berman EM Markets, Jupiter Gold & Silver, Oakley Capital Investments and TR Property. Our cash remains higher than average, ready to be reinvested during further market weakness.